Nvidia's Q2 Results Show Solid Performance but Moderating Growth; Here's What's Next

![]() FoolBull

FoolBull

23:10 August 27, 2025 EDT

Key Points:

For its fiscal second quarter 2026, NVIDIA's revenue increased 56% year-over-year (YoY) to $46.7 billion, while non-GAAP diluted EPS grew 54% YoY to $1.05. These results were primarily driven by strong demand in the Data Center segment, though they were also impacted by restrictions on sales to the Chinese market.

Since the generative AI boom began in mid-2023, NVIDIA's Q2 revenue growth of 56% marks its ninth consecutive quarter of exceeding 50% growth; however, it represents the slowest pace of expansion during this period.

Although NVIDIA’s performance this quarter did not deliver the significant upside surprise seen in prior periods, the company remains one of the few core beneficiaries directly leveraged to global AI infrastructure investment.

NVIDIA reported its fiscal Q2 2026 earnings after the U.S. market closed on August 27, 2025. While both revenue and profit exceeded market expectations, the stock declined more than 5% in extended trading.

Source: TradingView

Market concerns largely stem from NVIDIA’s core Data Center revenue coming in modestly below expectations, along with increasing uncertainties in the Chinese market. Additionally, although the 56% YoY revenue growth this quarter extends the streak of over-50% growth to nine consecutive quarters since the generative AI surge began in mid-2023, it also reflects the slowest growth rate in this period, raising investor apprehensions about a deceleration in momentum.

Key Financial Metrics

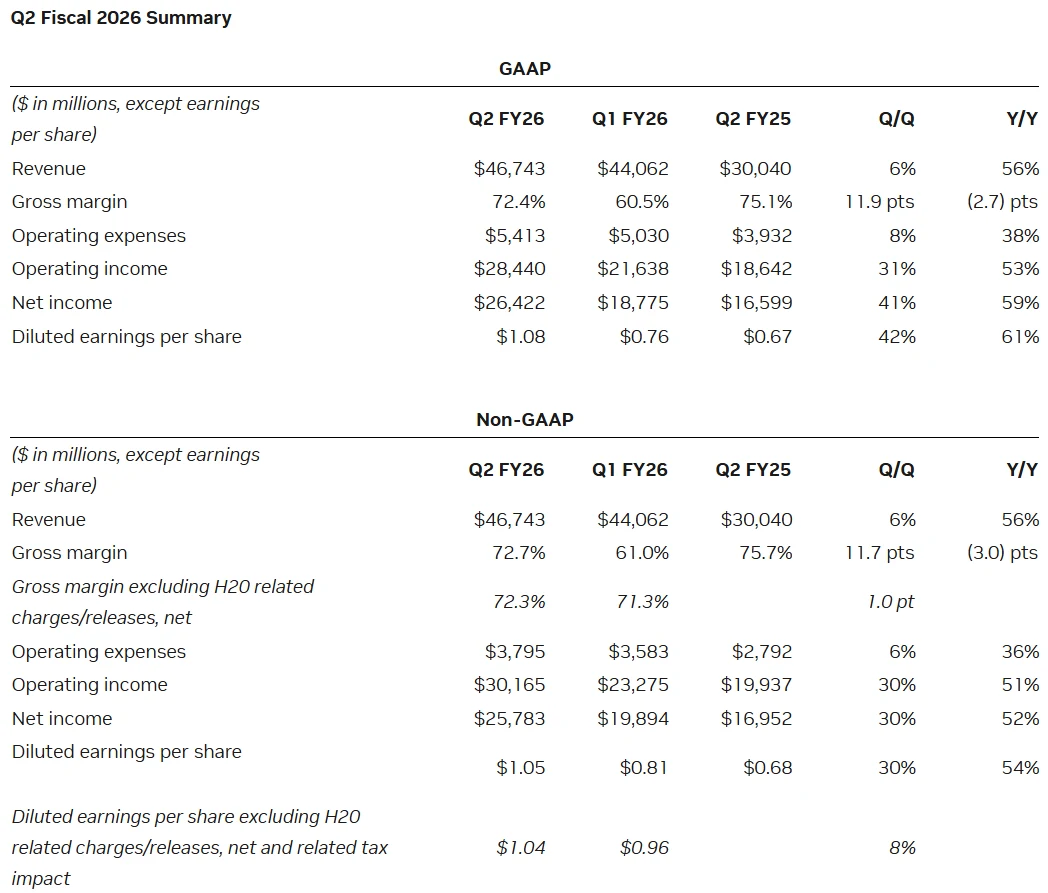

NVIDIA reported revenue of $46.743 billion for the second quarter of fiscal year 2026, representing a 56% year-over-year increase. This exceeded both analyst expectations of $46.23 billion and the high end of the company’s guidance range of $44.1 billion to $45.9 billion. The results extended NVIDIA’s streak of delivering over 50% year-over-year revenue growth for the ninth consecutive quarter since the generative AI wave began in mid-2023.

Source: NVIDIA

However, it is worth noting that the 56% year-over-year growth rate marks the lowest level during this period, down significantly from the 69% growth in the previous quarter, reflecting growth pressures under a high comparable base.

Source: NVIDIA

On the profitability front, non-GAAP adjusted earnings per share came in at $1.05, up 54% year-over-year and above the consensus estimate of $1.01. Excluding one-time impacts such as H20-related charges, EPS was $1.04, an 8% increase quarter-over-quarter, demonstrating the company’s effective cost control. Net profit reached $26.422 billion, a 59% year-over-year increase and higher than the market expectation of $23.465 billion, indicating sustained earnings quality.

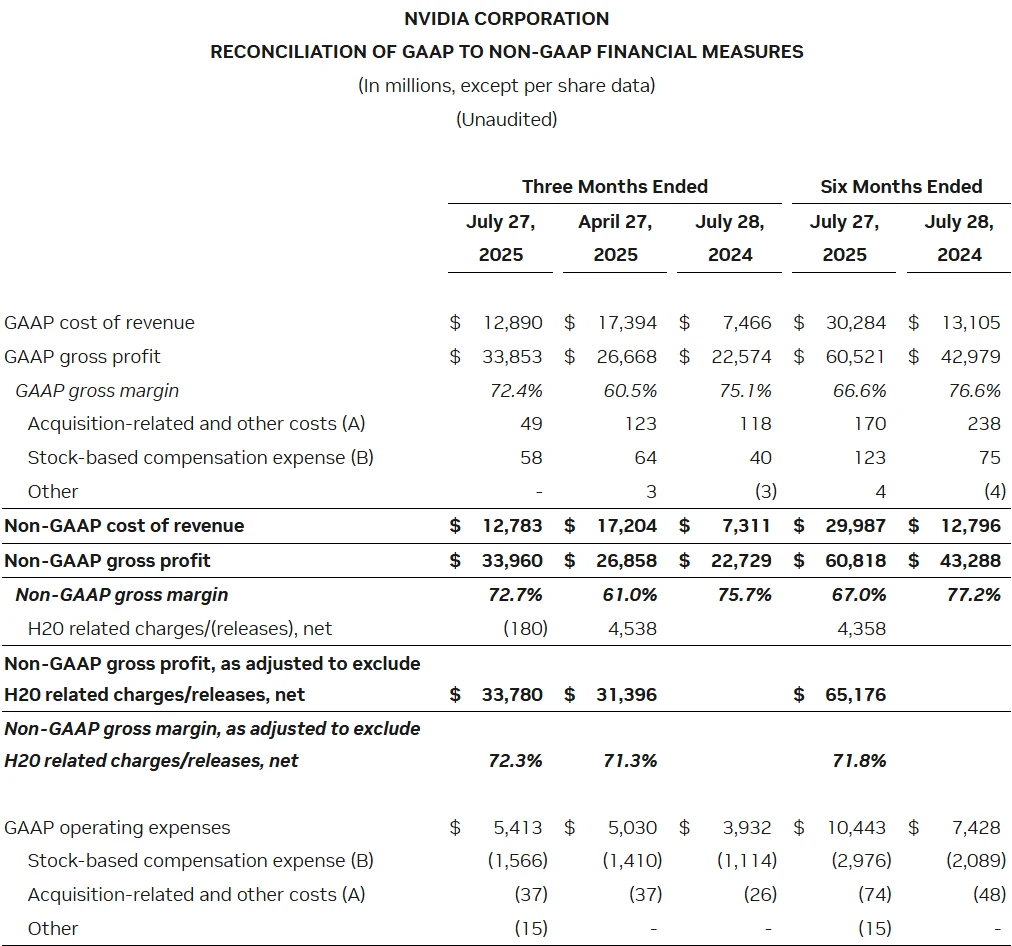

In terms of gross margin, the non-GAAP adjusted gross margin for the second quarter was 72.7%, down 3 percentage points year-over-year but exceeding both the analyst forecast of 72.1% and the upper end of the company’s guidance range of 71.5% to 72.5%. Excluding special impacts such as H20 inventory adjustments, the actual gross margin was 72.3%, up 1 percentage point quarter-over-quarter, indicating a recovery in core profitability. The company expects its non-GAAP gross margin to further improve to 73.5%, plus or minus 50 basis points, in the third quarter, reflecting confidence in product mix optimization.

Operating expenses were well-controlled, with adjusted operating expenses totaling $3.795 billion in the second quarter, up 36% year-over-year but below both the analyst estimate of $4.02 billion and the company’s own $4.0 billion guidance. The expense ratio—operating expenses divided by revenue—decreased to 8.1%, down from 9.4% in the previous quarter, highlighting improved operational efficiency driven by economies of scale.

Source: NVIDIA

Segment Performance

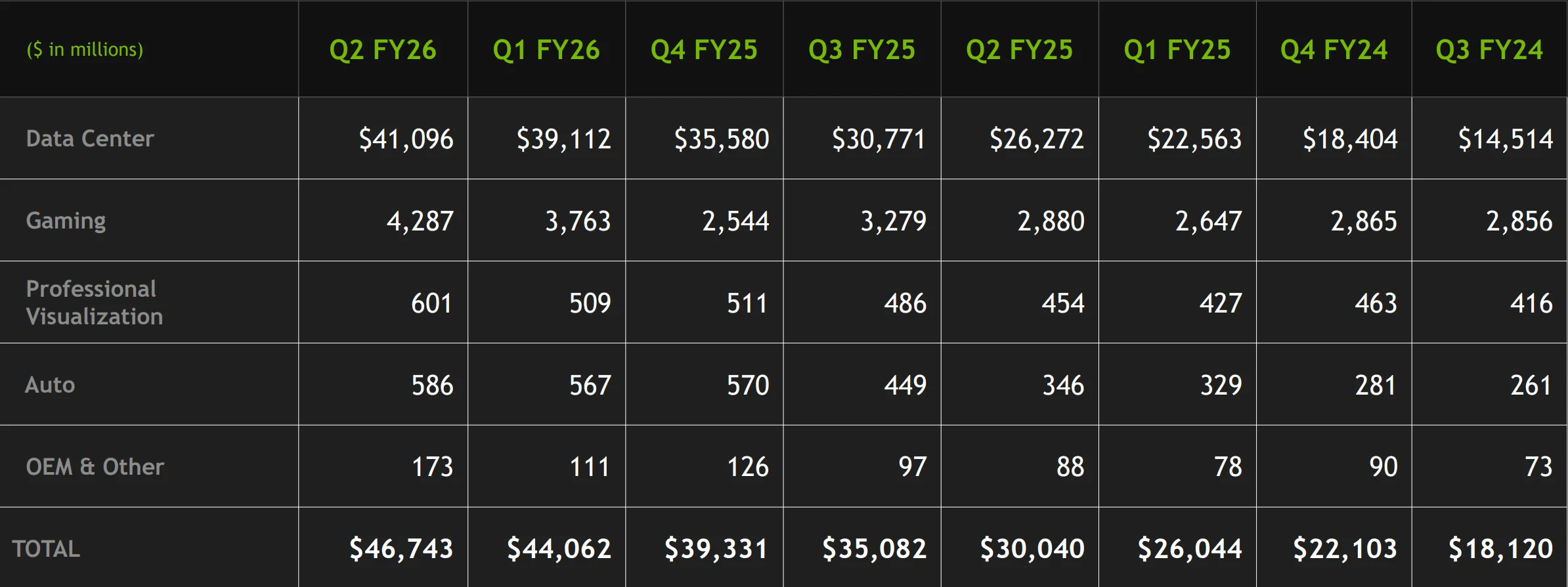

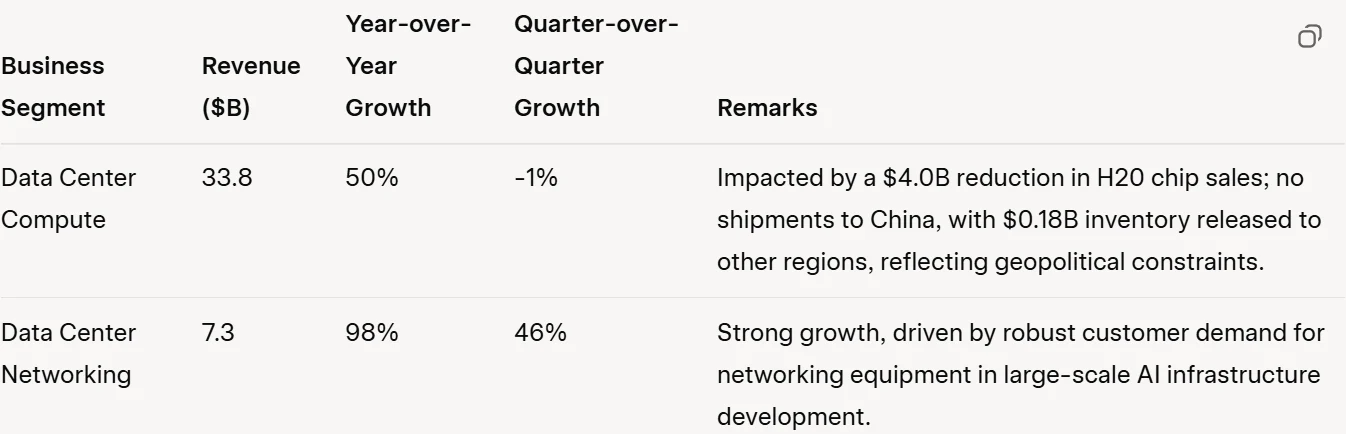

The Data Center segment remained the core growth driver for NVIDIA, generating $41.1 billion in revenue in the second quarter, a 56% year-over-year increase, accounting for 87.9% of total revenue. However, it fell modestly short of market expectations of $41.29 billion, which was a primary driver of the stock's volatility following the earnings release.

It is worth noting that performance within the segment showed significant divergence.

The new Blackwell architecture-based chips continued to demonstrate outstanding performance, with quarterly sales increasing 17% sequentially. The company has achieved a weekly production capacity of 1,000 racks, and large-scale cloud service providers contributed approximately 50% of the architecture’s sales. Disclosures revealed that Blackwell chip deliveries reached $11 billion in fiscal Q4 2025, setting a new record for NVIDIA in terms of new product revenue ramp, underscoring strong market acceptance of its technological evolution.

Although other business segments accounted for a relatively small share of total revenue, each maintained healthy growth:

Market Reaction

Following the earnings release, NVIDIA’s stock exhibited significant volatility. The stock closed slightly down 0.09% at $181.60 in the regular session, then fell more than 5% in after-hours trading before ending with a decline of 3.04%. This reaction is closely tied to market expectation management — although overall performance exceeded expectations, the slight miss in Data Center revenue and the deceleration in growth failed to satisfy investors’ entrenched expectation of consistent outperformance.

Nevertheless, this volatility aligns with NVIDIA’s historical post-earnings stock behavior. According to FactSet, the company has exceeded earnings expectations in 12 out of the past 13 quarters, yet the stock declined following the report on five of those occasions, reflecting how priced-in high expectations can trigger short-term sentiment swings.

Despite this, Wall Street analysts remain bullish on this AI leader. Goldman Sachs maintained its "Buy" rating and 12-month price target of $200, noting that NVIDIA’s results and guidance were largely in line but cautioning that near-term pressure may persist due to elevated expectations. Its report highlighted four key factors shaping NVIDIA’s trajectory: customer demand and supply chain dynamics, forward revenue and new products, the situation in China, and gross margin trends. Morgan Stanley acknowledged that uncertainties in China could lead to more conservative guidance but emphasized that its confidence in the long-term fundamentals remains unshaken.

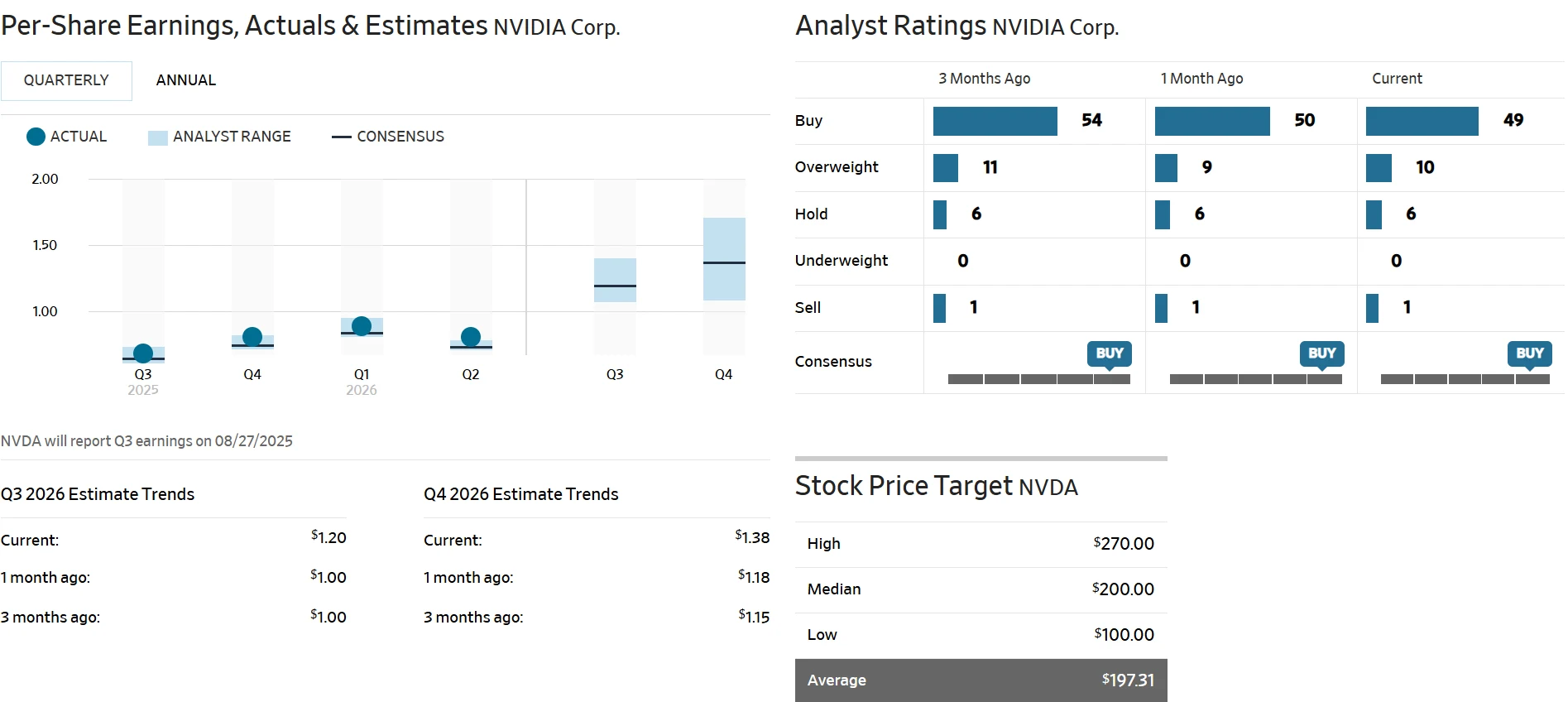

From a valuation perspective, as of the earnings release date, NVIDIA’s trailing twelve-month (TTM) P/E ratio stood at 58.58x, above the S&P 500 average. However, when considering its 56% revenue growth and 72.7% gross margin, its PEG ratio (Price/Earnings to Growth) remains within a reasonable range. The average price target among 66 analysts is $197.31, implying approximately 8.65% upside from the current level, indicating institutional confidence in its medium to long-term value.

Source: The Wall Street Journal

Behind this sentiment-driven volatility lie broader market concerns: whether AI infrastructure investment is facing cyclical slowing, when uncertainties in the Chinese market may ease, and whether the growth potential of Blackwell chips has already been fully priced in. These questions will continue to influence the direction of NVIDIA’s stock movement for the foreseeable future but are unlikely to alter its long-term growth trajectory.

Forward-Looking Commentary

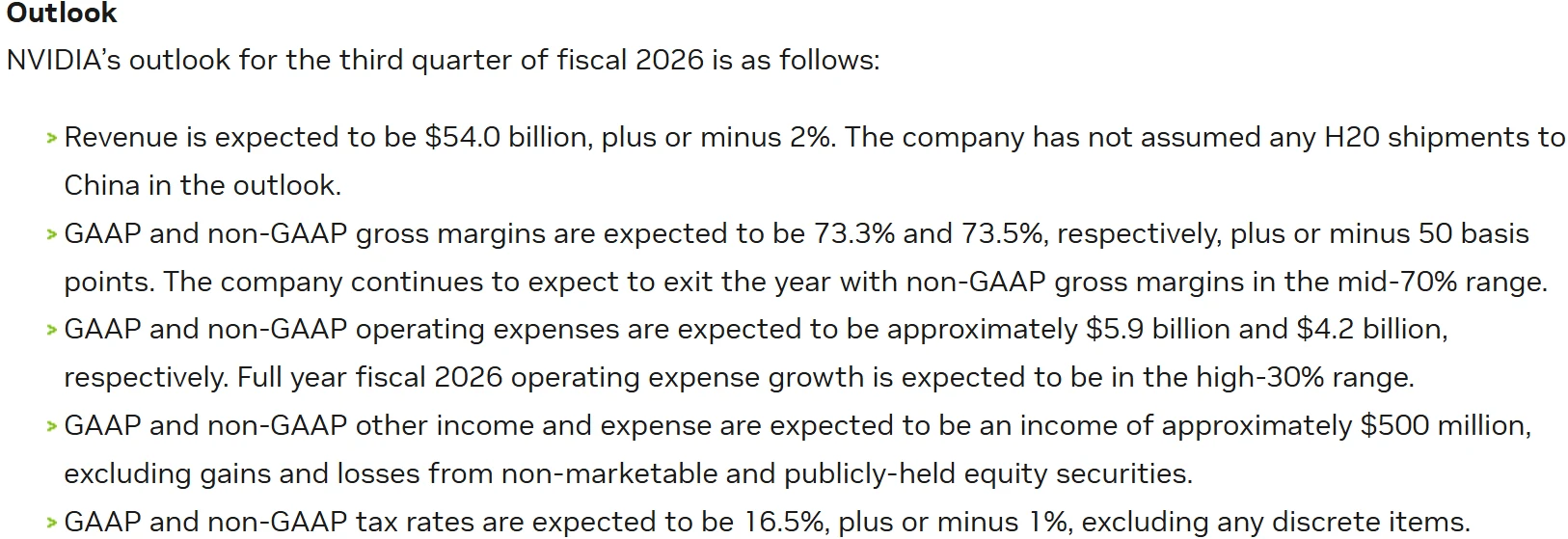

The company projects fiscal third-quarter revenue of $54 billion (±2%), implying a range of $52.92 billion to $55.08 billion, with the midpoint above the analyst consensus of $53.46 billion. The adjusted gross margin is expected to reach 73.5% (±50 bps), also exceeding market expectations of 73.4%. Operating expenses are anticipated to be $4.2 billion, with full-year growth expected at the high end of the “over 30%” range.

Source: NVIDIA

Notably, the company clarified that this guidance does not incorporate sales expectations for the H20 chips in the Chinese market. Should geopolitical conditions allow, H20 sales could contribute $2–5 billion in revenue in the third quarter. Some Chinese customers have already obtained licenses for H20 but have not yet commenced shipments, indicating potential upside should business conditions normalize.

During the earnings call, CEO Jensen Huang emphasized that the Chinese market could represent approximately $50 billion in commercial opportunity this year, noting that “there is a real possibility to bring Blackwell chips to China.” Historically, China contributed about 20% of NVIDIA’s Data Center segment revenue, and its recovery would significantly influence the overall growth trajectory.

Continued progression in the product cycle remains fundamental to NVIDIA’s long-term growth. Demand for the new Blackwell architecture-based GPUs remains robust, with quarterly sales growing 17% sequentially. CEO Jensen Huang stated that the company is “producing at full speed with exceptionally strong demand,” with initial customers including Disney, Hitachi, Hyundai Motor, and SAP. Furthermore, the market is closely monitoring the development of the next-generation Rubin architecture, which is expected to support revenue continuity beyond fiscal 2026.

Source: NVIDIA

Sustained growth in industry capital expenditure also indicates persistent AI demand, underpinning NVIDIA’s future growth. According to the CFO, global cloud service providers are projected to spend $600 billion on data center infrastructure and computing in 2025. Continued investment from major customers such as Microsoft, Amazon, and Meta is particularly critical—Microsoft’s Blackwell GB200 orders surged to 1,400–1,500 racks in Q4 2024, a 3–4x increase from previous levels, demonstrating leading clients’ long-term commitment to AI infrastructure.

Notably, against the backdrop of moderating growth in the Data Center segment, NVIDIA’s robotics business is emerging as a core future growth driver.

On August 22, NVIDIA announced that its robotics technology ecosystem now encompasses over 2 million developers. Subsequently, the company previewed and officially launched on August 25 a new computing platform designed specifically for humanoid robots—dubbed the “new brain.”

This system is based on Cosmos Reason, an open-source visual reasoning model unveiled at the SIGGRAPH conference on August 12. Cosmos Reason is a 7-billion-parameter visual-language model (VLM) that enables robots and AI agents to “reason like humans,” leveraging prior knowledge, physical understanding, and common sense to interpret and manipulate the real world. For example, in a demonstration, a robotic arm inferred that placing bread into a toaster was a logical next step given the context of “bread + toaster,” and translated that reasoning into operational commands.

Source: NVIDIA

Concurrently, NVIDIA has begun shipments of the Jetson Thor computing platform, engineered for physical AI and robotics applications. Based on the Blackwell architecture, Jetson Thor delivers 7.5x the AI compute performance and 3.5x the energy efficiency of its predecessor, Jetson AGX Orin. Initial adopters include leading global robotics companies such as Unitree Robotics, Zhiyuan Robotics, and Ubtech Robotics from China, alongside international players like Boston Dynamics, Agility Robotics, and Amazon Robotics.

Additionally, NVIDIA’s proactive capital allocation strategy warrants investor attention. The company repurchased $9.7 billion worth of shares in the second quarter, and the board authorized an additional $60 billion in share repurchases with no expiration date. This substantial buyback program not provides support for the share price but also reflects management’s confidence in the company’s valuation and its strong cash flow position.

Bottom Line

While NVIDIA’s performance this quarter did not deliver the significant upside surprise seen in previous periods, it still reflects the company’s dominant position in the AI computing market and strong operational execution. In the short term, the stock may face pressure due to moderated growth momentum and geopolitical uncertainties. Over the long term, however, its product competitiveness, customer ecosystem, and alignment with industry trends continue to support a constructive outlook.

Investors may consider initiating or increasing positions but should closely monitor subsequent earnings reports for updates on gross margin performance, recovery in the China business, and progress in next-generation products. NVIDIA remains one of the few core players directly benefiting from global AI infrastructure investment, and it continues to be a suitable holding for long-term investors with a certain tolerance for risk.

Disclaimer: The content of this article does not constitute a recommendation or investment advice for any financial products.

Email Subscription

Subscribe to our email service to receive the latest updates