With Fed Poised to Restart Rate Cuts, History Hints at Market Outcomes

![]() FoolBull

FoolBull

23:32 August 25, 2025 EDT

Key Points:

1. Federal Reserve Chair Jerome Powell's dovish remarks at the Jackson Hole Economic Symposium reinforced market expectations for interest rate cuts. Traders currently assign an approximately 80% probability to a 25-basis-point rate cut by the Fed in September.

2. If realized, this would constitute the first rate cut since December 2024, following a nine-month hiatus. Historical patterns indicate that U.S. equity markets have typically experienced short-term volatility but positive long-term performance following the initiation of a Fed easing cycle after a prolonged pause.

3. The Federal Open Market Committee (FOMC) is scheduled to convene on September 16-17. This meeting will release updated economic projections and the dot plot, serving as a critical juncture for assessing the validity of current market expectations.

In late August 2025, global financial markets focused on a potential pivot in the Federal Reserve's monetary policy. Fed Chair Jerome Powell's dovish stance at the Jackson Hole Economic Symposium drove market expectations for a September rate cut from around 65% to nearly 90%, signaling a possible end to the nine-month policy hiatus maintained since December 2024.

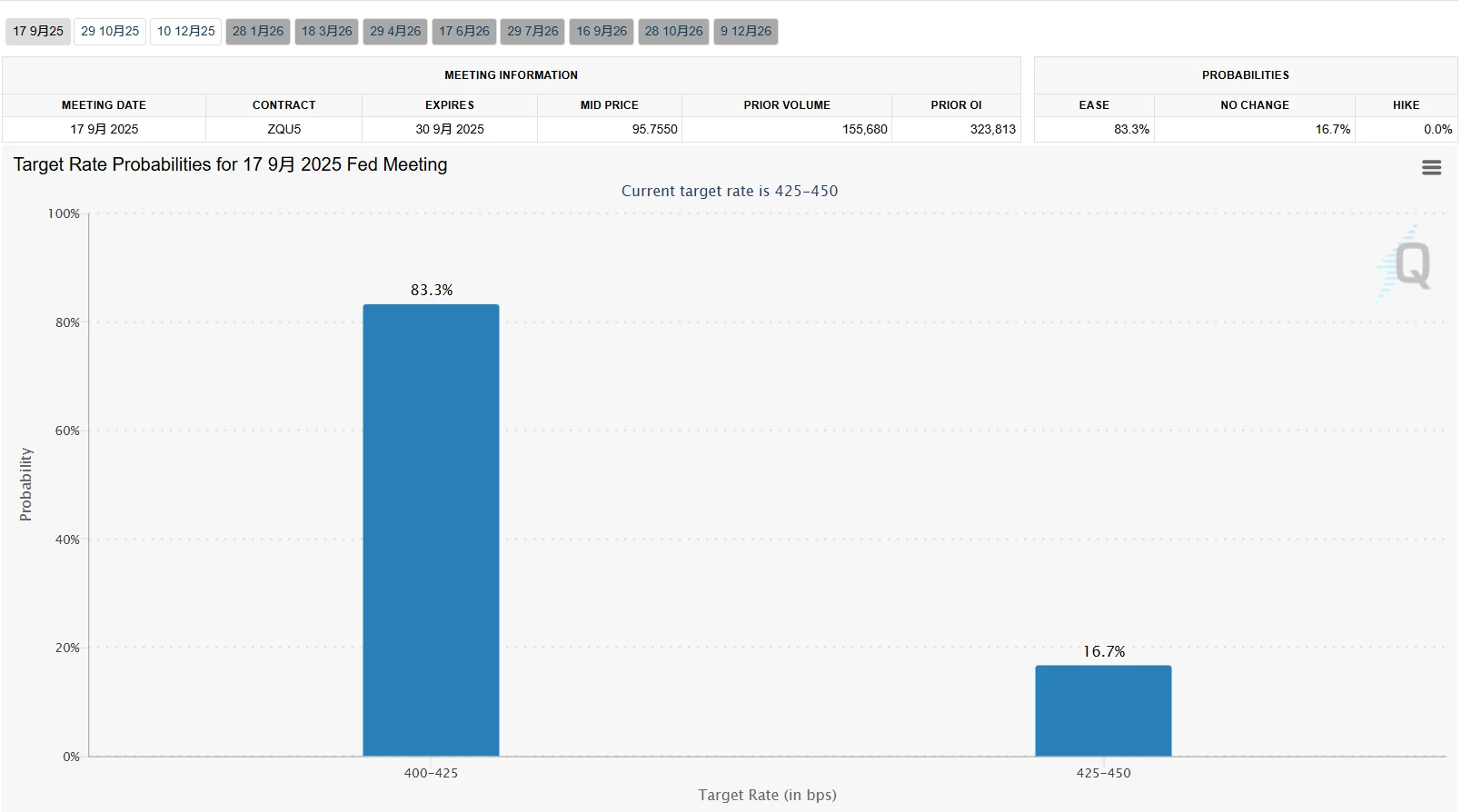

According to the CME FedWatch Tool, traders currently assign an 83% probability to a 25-basis-point rate cut in September, while the probability of at least two rate cuts within the year has also risen above 80%.

Source: CME

The Federal Open Market Committee (FOMC) is scheduled to convene on September 16-17. This meeting will release updated economic projections and the dot plot, serving as a critical juncture for validating market expectations. Should the rate cut expectations materialize, how might the markets respond?

Historical Precedents

Research from Ryan Detrick, Chief Market Strategist at Carson Group, reveals a consistent pattern: across 11 instances since 1970 where the Fed resumed rate cuts after a 5-12 month pause, the S&P 500 declined by an average of 0.9% one month after the cut and 1.3% after three months. However, it registered gains in 10 of those periods over the subsequent year, with an average increase of 12.9%.

Source: FRED

This data illustrates the market’s typical reaction to a policy pivot—short-term profit-taking pressure as expectations are realized, followed by longer-term benefits from the systematic support of an accommodative environment for the economy and corporate earnings.

LPL Financial’s research further expands this perspective. Across nine full easing cycles since 1974, the S&P 500 delivered an average return of 30.3%, with positive returns in six of those cycles. However, performance varied significantly depending on the economic backdrop: it surged 161% during the 1995-1999 internet boom but fell 23.5% during the 2007-2009 financial crisis, indicating that the effectiveness of rate cuts is closely tied to the underlying health of the economy.

Source: TradingView

The 2019 preemptive rate cut cycle offers a particularly relevant reference point. Similar to the current environment, the U.S. economy was not in recession in 2019, but nonfarm payroll growth had slowed—averaging 178,000 per month, down from 223,000 in 2018. With core PCE inflation stable in the 1.5%-1.8% range, this combination of "weaker employment and subdued inflation" created the conditions for preemptive rate cuts.

Source: FRED

At that time, the Fed resumed cutting rates after a 10-month pause. The S&P 500 rose 29% for the year, and the Nasdaq Composite gained 35%, characterized by leadership from growth stocks. This backdrop—an economy avoiding recession amid a softening labor market—closely mirrors current conditions and provides a positive historical reference. In contrast, during the 2001 dot-com bust, the S&P 500 still fell 9.6% despite aggressive Fed rate cuts, demonstrating that monetary policy effectiveness is significantly constrained when economic fundamentals deteriorate severely.

Source: TradingView

The current economic conditions

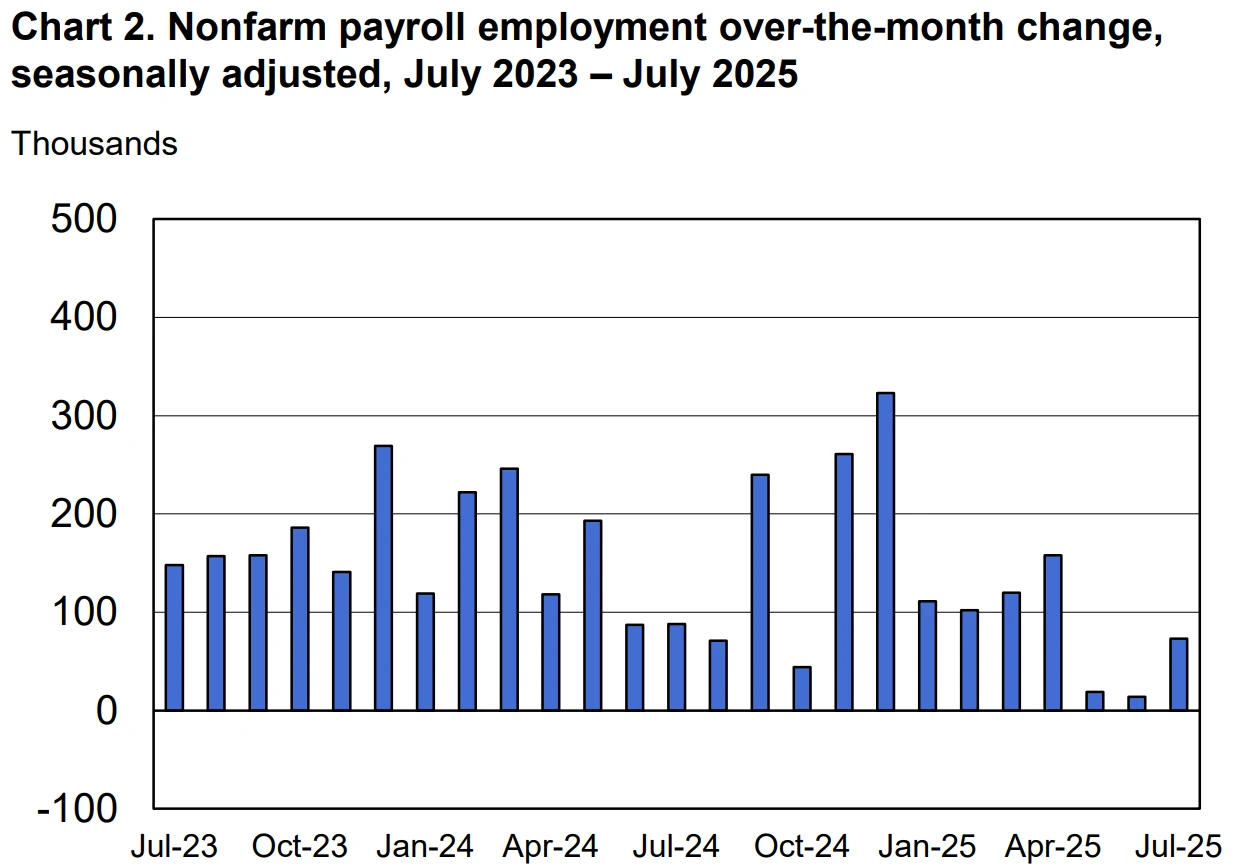

The July 2025 U.S. nonfarm payroll data served as a key catalyst reinforcing expectations for interest rate cuts. The economy added just 73,000 jobs during the month, falling significantly short of market expectations of 110,000. Furthermore, data for May and June was revised downward by a combined 258,000, pulling the three-month average job gain down to 35,000—well below the 100,000 threshold typically associated with healthy labor market expansion.

Source: Bureau of Labor Statistics (BLS)

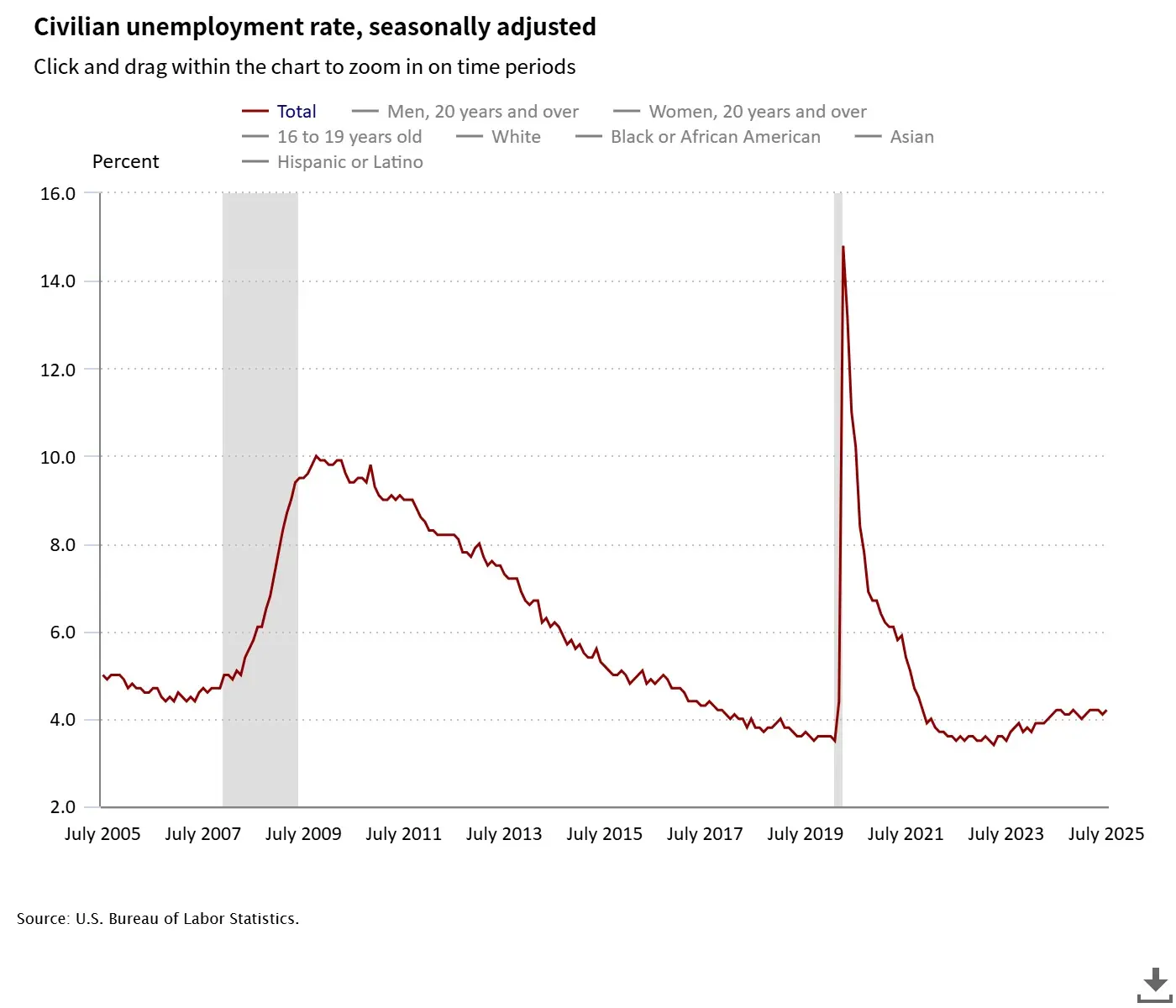

The unemployment rate climbed to 4.2%, while continuing jobless claims rose to 1.972 million, the highest level since November 2021. These figures clearly indicate intensifying downside risks in the labor market.

Source: Bureau of Labor Statistics (BLS)

On the inflation front, core CPI increased 3.1% year-over-year in July. While this remains above the Federal Reserve's 2% target, it represents a notable decline from its peak in 2024.

Source: Bureau of Economic Analysis (BEA)

In his Jackson Hole speech, Chair Powell outlined a "reasonable baseline assumption" that the inflationary impact of tariffs would be one-time in nature and would take time to fully materialize. This assessment provided a theoretical foundation for potential rate cuts. The current combination of a cooling labor market and moderating inflation mirrors the economic conditions preceding the preemptive rate cuts in 2019, creating a suitable environment for policy adjustment.

Internal divisions within the Fed regarding the appropriate policy path have further complicated market expectations. During the July FOMC meeting, two Governors—Waller and Bowman—cast rare dissenting votes, advocating for an immediate 25-basis-point rate cut. This marked the first instance of two Governors simultaneously dissenting on a rate decision since 1993. Dovish members argue that high interest rates are already suppressing employment and economic vitality, while hawkish members remain concerned that tariffs could exert upward pressure on inflation.

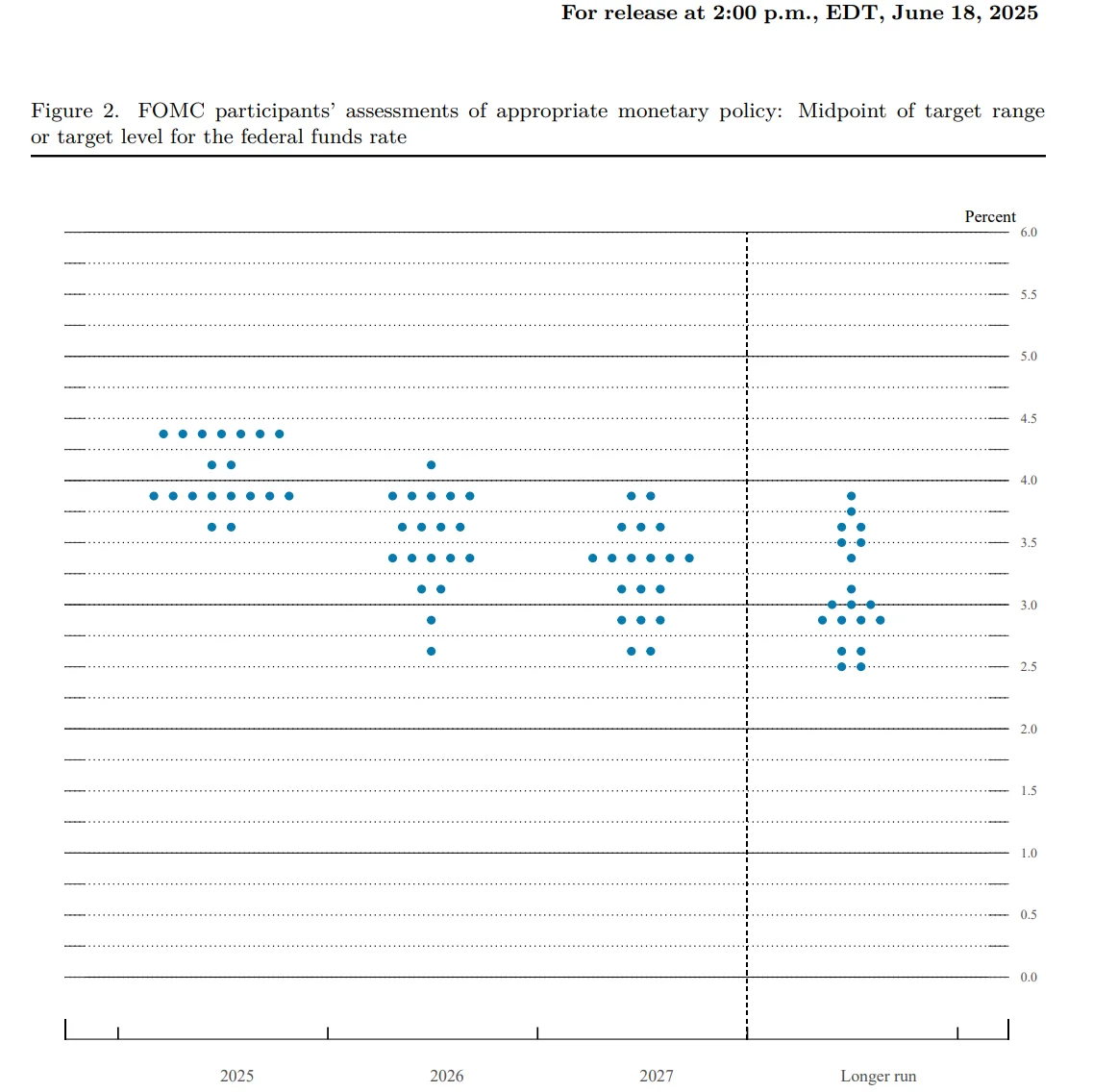

According to the dot plot released in June, the median projection among Fed officials anticipates two rate cuts in 2025. Eight of the 19 officials supported this view, two projected three cuts, while seven argued for no rate cuts at all. This divergence suggests the potential for even greater disagreement at the September meeting, where subtle changes in the policy statement and dot plot are likely to significantly impact market sentiment.

Source: Federal Reserve

Market Developments

Rising expectations for interest rate cuts have already triggered shifts in the U.S. equity market.

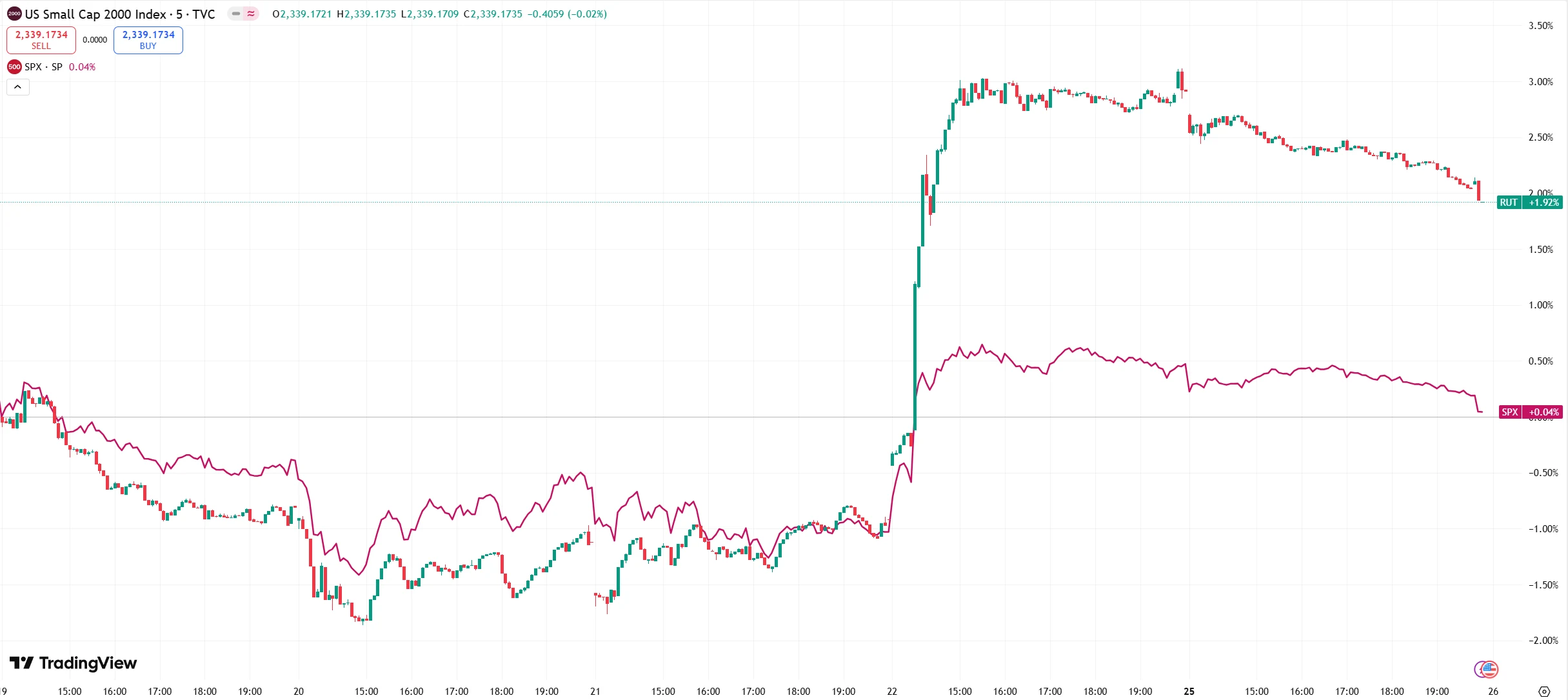

High-sensitivity sectors reacted first. The Russell 2000 small-cap index surged 3.9% in a single day following Powell's Jackson Hole speech, significantly outperforming the S&P 500's 1.5% gain. These companies typically carry more floating-rate debt and are more sensitive to changes in borrowing costs. Lower interest rates directly reduce their financing expenses and improve profitability. Historical data show that the Russell 2000 has tended to outperform the broader market by 5-8 percentage points in the year following the resumption of a rate-cutting cycle.

Source: TradingView

Growth stocks face a test of valuation and earnings rebalancing. The technology sector of the S&P 500 currently trades at a forward P/E ratio of 30x, near its one-year high. However, its EPS growth of 24.6% year-over-year significantly outpaces the 5.9% growth in the rest of the market, indicating that valuations are partially supported by fundamentals. While a low-rate environment reduces the discount rate for future cash flows—theoretically supporting growth stock valuations—Mike Reynolds, VP of Investment Strategy at Glenmede, notes that upside may be limited if earnings growth fails to justify elevated valuations.

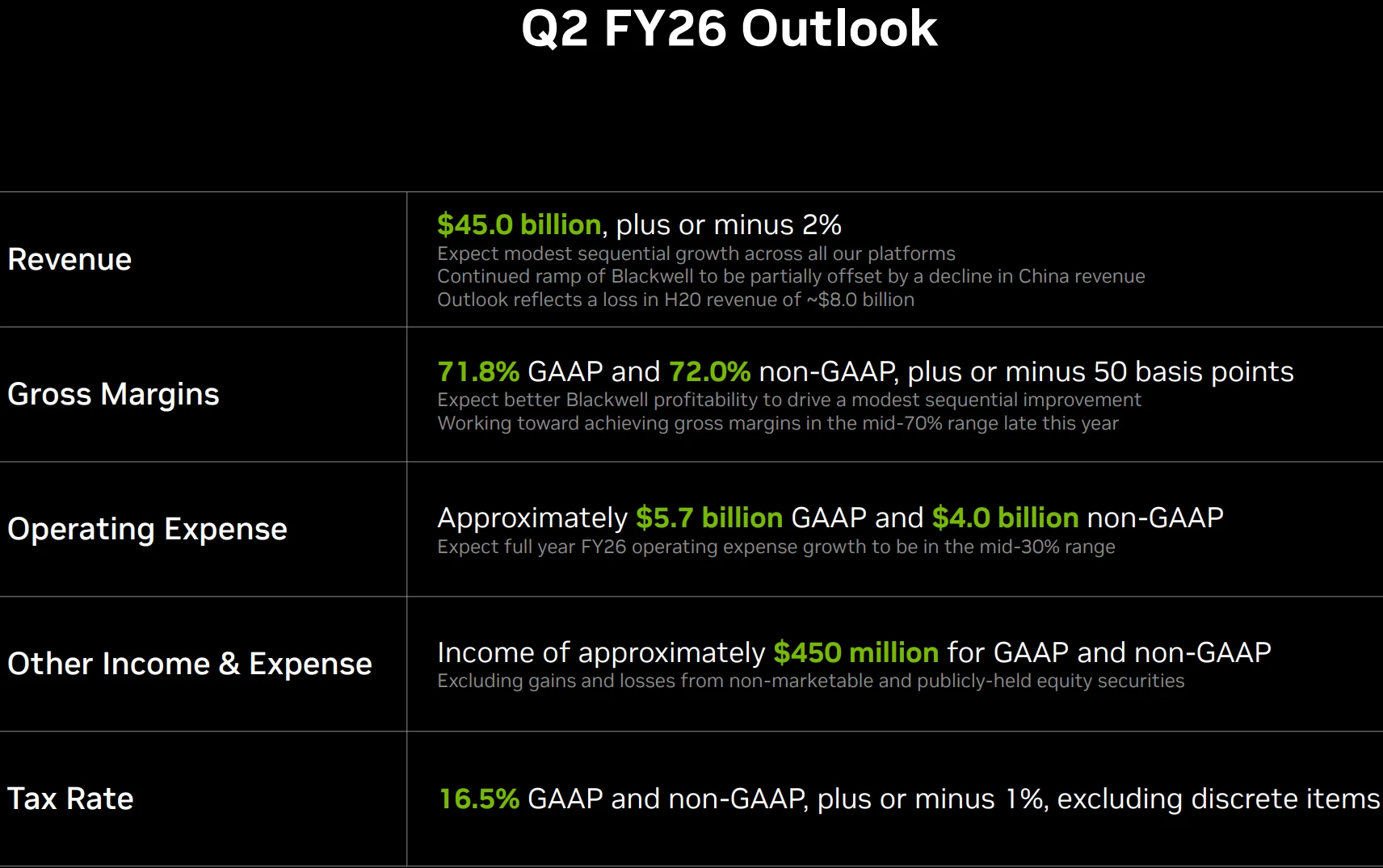

The earnings reports of AI leaders like NVIDIA will serve as a critical bellwether, amid market concerns that the AI spending boom may show signs of slowing. Within the S&P 500 technology sector, AI-related companies account for 35% of earnings growth. As the leading AI chip manufacturer, NVIDIA’s revenue guidance and gross margin data will directly influence market perceptions of AI demand and impact the valuation logic for growth stocks.

Source: NVIDIA

Cyclical sectors are showing signs of recovery. Industrial metals and basic materials may benefit from a weaker U.S. dollar and improved demand expectations. Rate cuts are typically accompanied by dollar weakness—the U.S. Dollar Index has already retreated to around 98 from its yearly high, a 13-month low—which would enhance the price competitiveness of dollar-denominated commodities.

Source: TradingView

The financial sector faces a mixed outlook of narrowing net interest margins and potential credit expansion. Bank stocks, particularly regional banks with higher reliance on net interest income, will face near-term pressure on margins. However, over the longer term, a recovery in credit demand may partially offset these headwinds.

Steve Sosnick, Chief Strategist at Interactive Brokers, notes that assets further out on the risk curve generally perform better as rate cut expectations rise. This pattern has already seen preliminary validation: beyond small caps, growth stocks with high technological barriers—such as semiconductor equipment and AI infrastructure providers—have also demonstrated strong resilience. In contrast, defensive sectors like utilities and consumer staples may relatively underperform.

Underlying Risks

Despite strong expectations for interest rate cuts, the market continues to face multiple sources of uncertainty. The primary risk remains the potential for policy actions to fall short of market expectations. While current pricing suggests an 83% probability of a 25-basis-point cut in September, institutions like Morgan Stanley and Bank of America maintain that the Fed will hold rates steady, arguing that more evidence of economic softening is needed.

Historical experience serves as a cautionary reminder. In September 2007, the Fed executed a 50-basis-point cut—lowering the federal funds rate from 5.25% to 4.75%—in response to the emerging global financial crisis triggered by the subprime mortgage collapse. In the two weeks following that decision, the S&P 500 rallied 6%. However, from September 2007 through its trough in March 2009, the index ultimately declined approximately 56%, as the severity of the subprime crisis far exceeded initial expectations.

Source: TradingView

Unexpected volatility in economic data could alter the policy trajectory. Key incoming data—including July’s PCE inflation reading (the Fed’s preferred inflation gauge) and August’s nonfarm payrolls report—will heavily influence the Fed’s decision. A rebound in inflation or unexpectedly strong employment data could delay the timing of rate cuts. The core CPI reading for July 2025, which rose 0.3% month-over-month and slightly exceeded expectations, briefly dampened market sentiment—demonstrating the acute sensitivity of policy expectations to economic releases.

Trade policy uncertainty further complicates the economic outlook. The potential implementation of new tariff regimes could directly impact multinational corporate profits. Jeff Buchbinder, Chief Equity Strategist at LPL Financial, warns that a new tariff system—unprecedented since the 1930s—could slow earnings growth and amplify market volatility. Goldman Sachs similarly estimates that a 5-percentage-point increase in effective U.S. tariff rates could reduce S&P 500 earnings per share (EPS) by approximately 1-2% in 2025.

Chair Powell specifically noted that 30% to 40% of current core inflation may be attributable to tariffs. This lagging effect complicates the Fed’s policy decisions and introduces additional uncertainty into the market.

Valuation pressures present another latent risk. The S&P 500’s current price-to-earnings ratio sits at the 75th percentile historically, with technology stock valuations at particularly elevated levels. Should earnings growth fail to meet expectations following rate cuts, a valuation correction could ensue. The precedent of the dot-com bust in 2000—during which the Nasdaq Composite fell 39.3% despite aggressive Fed easing—serves as a stark reminder that high valuations amid unmet earnings expectations can significantly amplify market downturns.

Final Thoughts

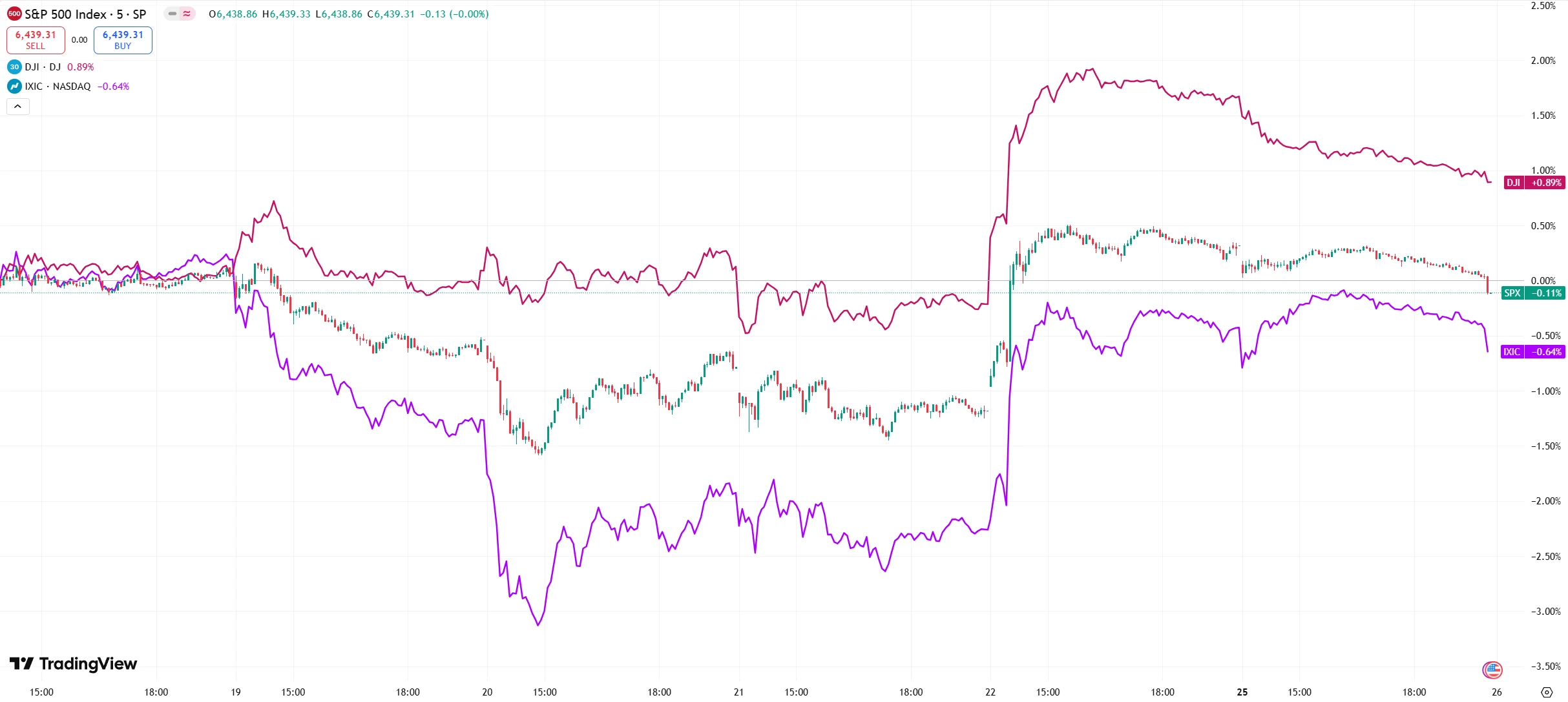

U.S. major indices closed lower across the board by Monday’s market close—the Dow Jones Industrial Average fell 0.77%, the S&P 500 declined 0.43%, and the Nasdaq Composite dropped 0.22%. The pullback tempered the market’s upbeat momentum following Fed Chair Jerome Powell’s remarks last Friday, which had sharply raised expectations for a September rate cut and driven a substantial rally. During that session, the Dow climbed to a record high.

Source: TradingView

The market now awaits the release of July’s Personal Consumption Expenditures (PCE) data this Friday—the Federal Reserve’s most closely watched inflation gauge. Historical data consistently point in one direction: within one year after the Fed resumes rate cuts, the S&P 500 has risen in 10 out of 11 instances, with an average gain of 12.9%.

Investors have already begun positioning. Historical patterns suggest that if the Fed cuts rates in September, the S&P 500 may face corrective pressure over the following one to three months, likely reflecting profit-taking as expectations are realized. However, over a longer horizon, the odds of gains stand above 90%, underscoring the systematic support provided by an accommodative policy environment.

Disclaimer: The content of this article does not constitute a recommendation or investment advice for any financial products.

Email Subscription

Subscribe to our email service to receive the latest updates