Will This Classic Investment Strategy Still Deliver for Investors in 2025?

![]() FoolBull

FoolBull

06:21 August 25, 2025 EDT

In 2022, the global financial markets experienced a “double hit” in both equities and bonds, as major central banks simultaneously raised interest rates to combat high inflation, leading to concurrent declines in stock and bond prices. In the U.S., the 60/40 investment portfolio (60% equities + 40% bonds) recorded an annual loss of 16%, the largest since 1976, raising widespread doubts about the effectiveness of this strategy and significantly undermining investor confidence.

Entering 2025, global markets continue to face multiple challenges: the Trump administration raised average tariffs on imported goods to 15%, increasing inflation persistence in the U.S. and adding to global trade uncertainty; global supply chain restructuring persists, with semiconductor and new energy industry chains becoming regionally concentrated, causing corporate profits to be affected by production costs and raw material fluctuations; growth among major economies remains uneven, with the U.S. relying on moderate consumer expansion, the eurozone stagnating due to rebounding energy prices, and emerging markets showing differentiated recoveries linked to commodity prices; geopolitical tensions in the Middle East and Eastern Europe continue to disrupt global energy supply and risk appetite.

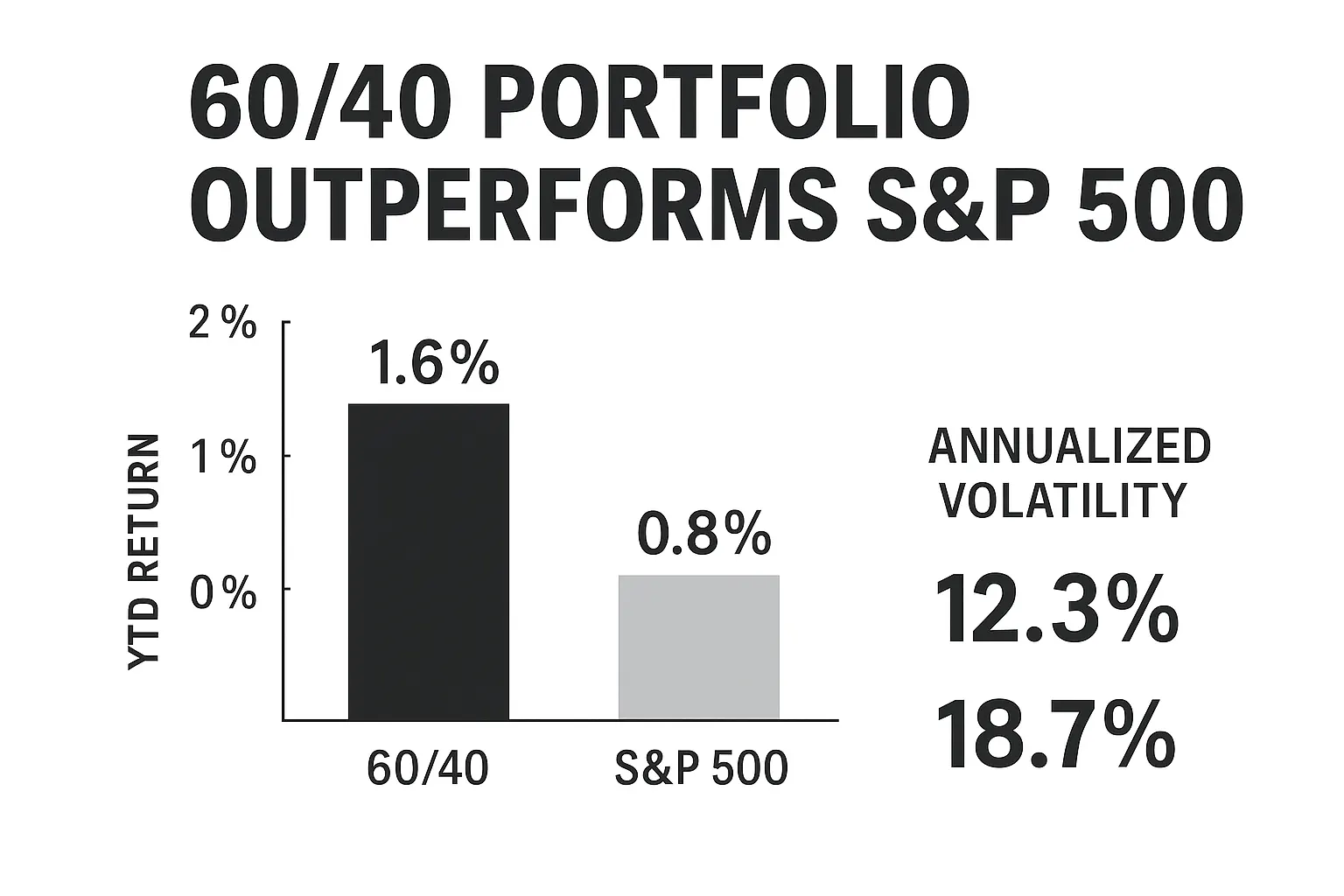

Against this backdrop, the 60/40 strategy has shown improved performance: the traditional negative correlation between equities and bonds has normalized after the abnormal conditions of 2022, and price volatility correlations have returned to typical levels. As of the end of July 2025, a portfolio consisting of 60% S&P 500 Index and 40% Bloomberg U.S. Aggregate Bond Index has returned approximately 1.6% year-to-date, outperforming the S&P 500 Index by 0.8 percentage points; the annualized volatility is 12.3%, significantly lower than the roughly 18.7% of a pure equity portfolio.

This report will evaluate the 60/40 strategy’s profit potential from four perspectives: the differentiated market performance characteristics in 2025, verification of the strategy’s core logic, the impact mechanisms of the macro environment on the strategy, and the dynamic optimization path of the strategy. It will also take into account the unique conditions of the global markets in 2025, providing a reference for asset allocation decisions for investors with varying risk preferences.

Market Validation

In the first half of 2025, the 60/40 investment portfolio exhibited a “recovery but differentiated” pattern. Overall, after the 16% annual decline in 2022, the strategy has posted positive returns for three consecutive years, and cumulative returns since the 2022 trough have reached a notable level, demonstrating strong resilience. The core driver of this recovery is the restoration of the traditional inverse relationship between stocks and bonds — over the past six months, the correlation between U.S. equities and fixed income has fallen to its lowest level since 2021. This means that when stocks decline, bonds tend to rise, and vice versa, which is the fundamental premise for the effectiveness of the 60/40 strategy.

However, there is significant internal differentiation in the strategy’s performance. In the equity portion, global markets have shown an “East up, West down” pattern. In Q1 2025, the S&P 500 underperformed non-U.S. equities (measured by the MSCI ACWI ex-USA Index) by nearly 11 percentage points, marking the largest relative outperformance by non-U.S. stocks over U.S. stocks in any first quarter on record.

Source: MSCI

The strong performance in non-U.S. markets has been driven primarily by a weaker U.S. dollar and differences in regional economic recovery momentum, with Germany’s DAX 40 and Hong Kong’s Hang Seng Index standing out. According to Hong Kong Exchange data, the Hang Seng Index has risen over 20% so far in 2025.

Source: TradingView

In the bond portion, a “strong short, weak long” pattern has emerged. Prices of benchmark 30-year U.S. Treasuries have fallen sharply, pushing yields above 5%, near a twenty-year high, while short-term bonds have remained relatively stable. This differentiation has led to what Wall Street describes as “yield curve steepening” — as the 30-year Treasury yield surged over 25 basis points year-to-date, two- and five-year Treasury yields declined simultaneously, reflecting investor preference for short-term bonds to mitigate long-term deficit risks.

Source: TradingView

Data show that in the first half of 2025, U.S. Treasuries recorded the strongest performance in five years. The Bloomberg U.S. Aggregate Treasury Index returned nearly 1% in June, and by the end of July, the overall performance of U.S. Treasuries for the year remained positive, with most gains coming from short- and intermediate-term securities.

The Core Logic

The improvement in the 60/40 strategy’s performance in 2025 is primarily driven by the restoration of the negative correlation between stocks and bonds, allowing the underlying logic of the strategy to function effectively again. Some analysts note that “over the long term, balanced allocation does make sense.” This significance is particularly evident during periods of market volatility.

Globally, the “see-saw effect” between stocks and bonds has been pronounced in 2025.

In the U.S. market, the negative correlation between equities and bonds is observable — for example, when the S&P 500 experiences significant declines, 10-year Treasury yields tend to fall. This effect was especially notable in April: during the equity market rally driven by AI-related stocks, bond indices fell slightly, but when equities corrected in May, bonds rebounded rapidly, providing a near-perfect hedge.

Source: TradingView

Historical data further supports the stability of this logic. PIMCO research shows that over the past 40+ years, the 60/40 portfolio has historically generated positive returns in most rolling three-year periods, with only a few exceptions occurring in extreme market environments. The strategy performs particularly well during rate-cut cycles.

Looking at historical rate-cut cycles, the yield on the U.S. 10-year Treasury has declined on average by 0.2%, 0.3%, and 0.3% within 30, 60, and 180 days, respectively, following the first rate cut. Chinese bonds also showed declining rates during some rate-cut periods.

In terms of return characteristics, the strategy achieves “nonlinear optimization of risk and return.” Although overall stock market valuations remain elevated in 2025, with the S&P 500 earnings yield falling to 3.95%, roughly half a percentage point below the 10-year Treasury yield, the stock-bond balance allows the portfolio to generate reasonable returns while controlling risk. Current valuations suggest a long-term expected return for equities of approximately 6%–7%, compared with an average yield of around 4.8% for the Bloomberg U.S. Aggregate Bond Index. While the relative advantage has narrowed, the strategy still retains allocation value.

Policy Shift

Major shifts in global macroeconomic policy in 2025 have introduced new variables for the 60/40 strategy.

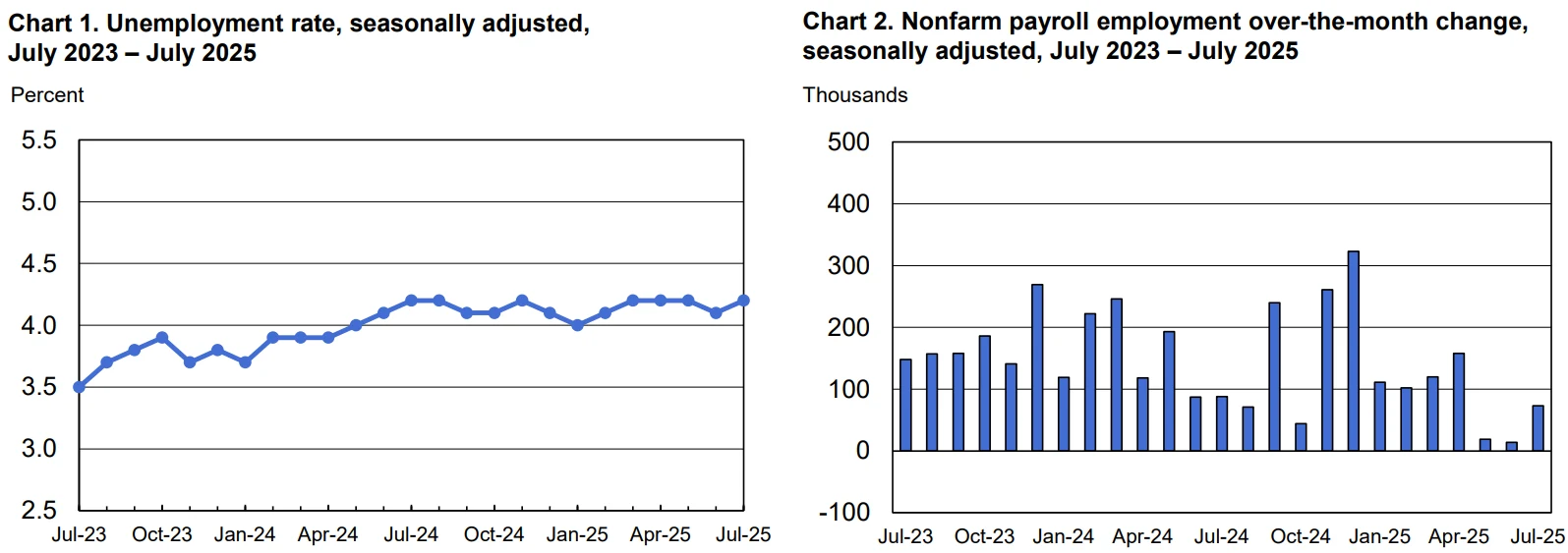

On August 22, Federal Reserve Chair Jerome Powell delivered a clearly dovish signal at the Jackson Hole Global Central Banking Symposium, stating that “changes in the baseline outlook and risk balance may require adjustments to our policy stance.” Powell noted that the U.S. labor market is in a “fragile balance” with both supply and demand weakening, and downside risks to employment are rising. The July nonfarm payrolls data were sharply revised down, showing only 35,000 new jobs, far below the 2024 monthly average of 168,000.

Source: U.S. Bureau of Labor Statistics

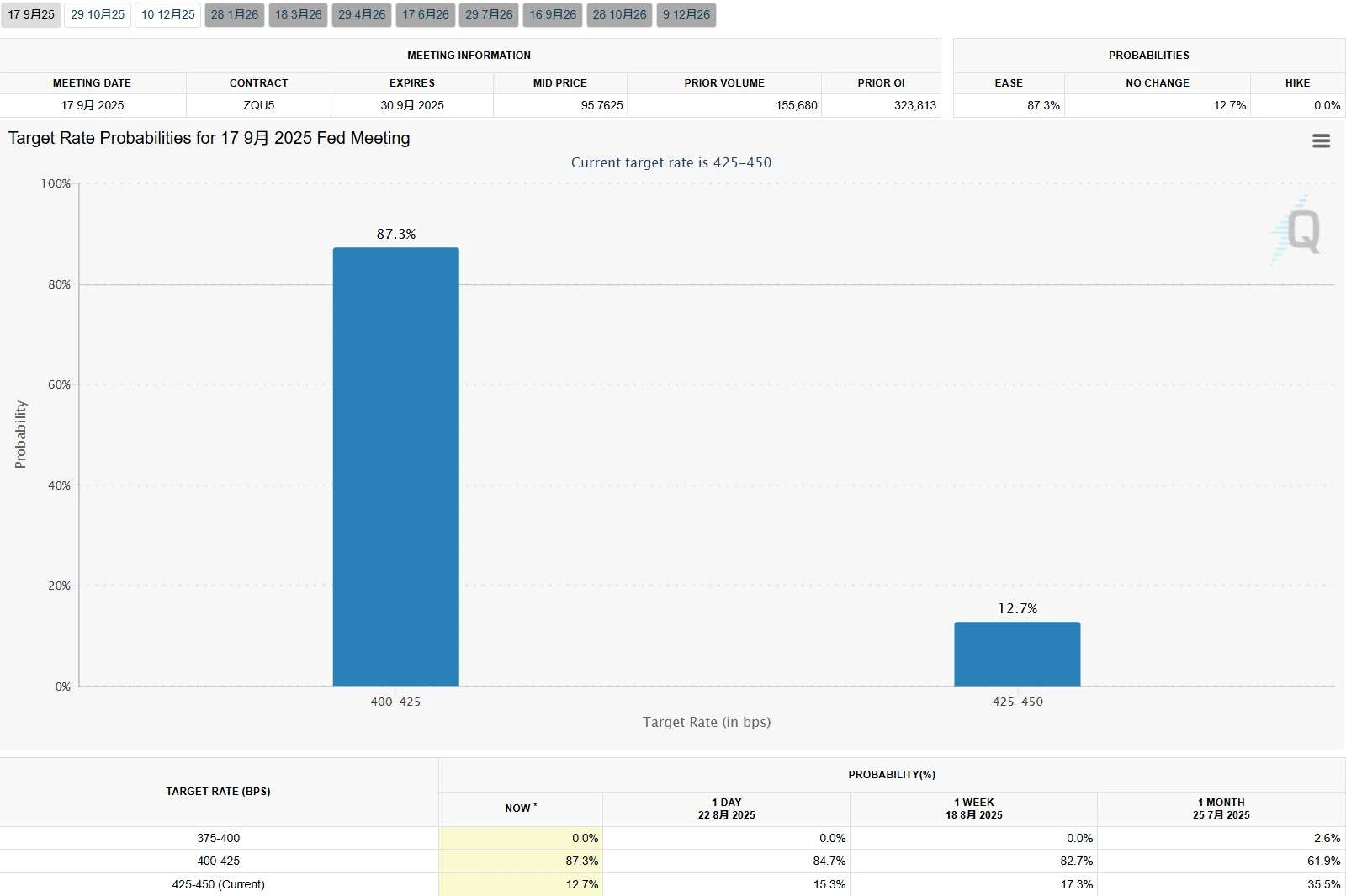

This statement triggered strong market expectations of a Fed policy shift toward easing. According to the CME FedWatch Tool, after Powell’s speech, traders increased the probability of a 25-basis-point rate cut in September from around 65% to 87%. Multiple investment banks, including Barclays, BNP Paribas, and Deutsche Bank, now expect a 25-basis-point rate cut at the September FOMC meeting, followed by another cut in December.

Source: CME

This policy shift has significant implications for both core asset classes in the 60/40 portfolio.

For the bond market, the rate-cut expectations are broadly supportive but show structural differentiation. In theory, short-term bonds benefit most, as the expected economic slowdown and Fed easing favor the short end of the yield curve. In practice, however, at the close in New York on August 21, the two-year Treasury yield rose 4.40 basis points to 3.7918%, and the five-year yield rose 4.37 basis points, contrary to the expected decline under a rate-cut scenario. Long-term bonds, while influenced by concerns over fiscal deficits, remained below key thresholds, with the 30-year Treasury yield at 4.95% as of July 29, 2025. This complex market environment highlights the need for more refined duration management in bond allocations rather than a simple 40% fixed allocation.

In equities, markets faced a scenario of “high valuations amid policy tailwinds.” Expectations of Fed easing triggered a significant rebound in U.S. stocks after Powell’s speech. By the close of New York trading on August 22, the U.S. dollar index fell 0.94% to 97.72, providing some support for multinational earnings.

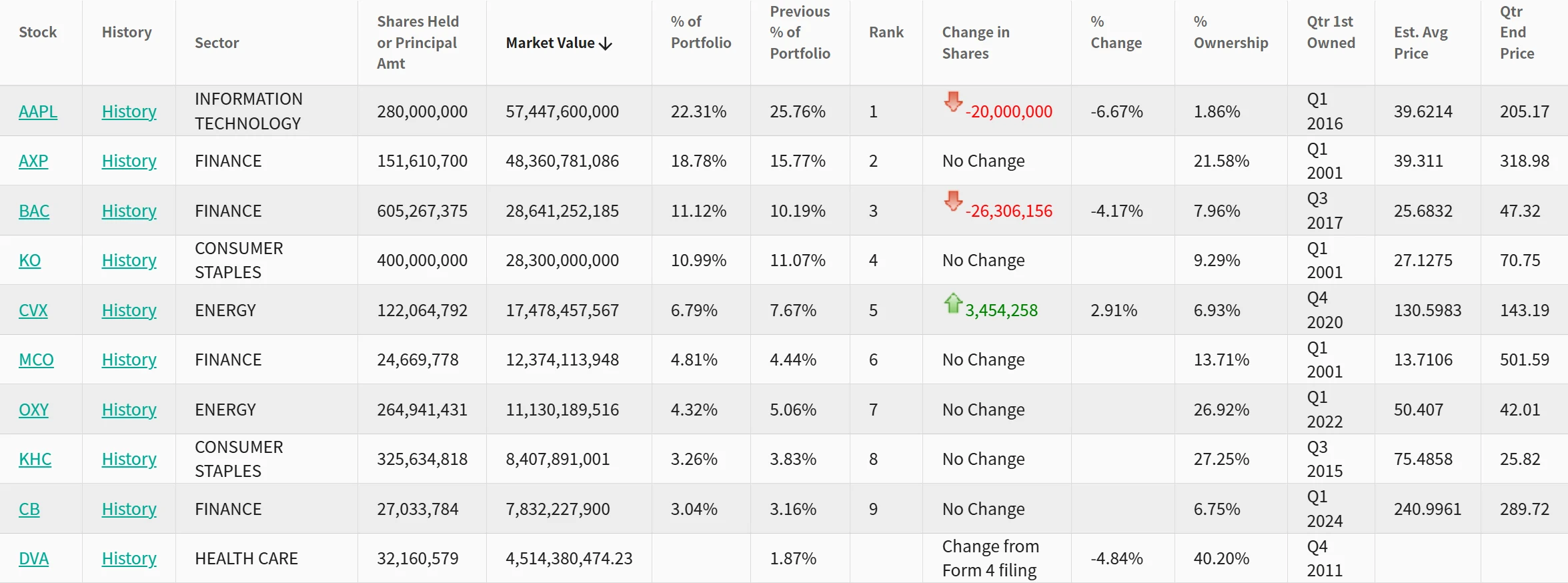

However, the S&P 500 remains at elevated valuations. Warren Buffett reduced holdings in Apple, Bank of America, and other stocks in Q2 2025 but also initiated positions in Nucor and UnitedHealth, indicating that U.S. equity exposure was not being broadly reduced. This mixed approach underscores the need for global diversification in equity allocations rather than reliance on the U.S. market alone.

Source: WhaleWisdom

It is also important to note that different markets are responding differently to Fed policy.

In the U.S., markets currently price in the potential for roughly 125 basis points of cuts by the end of next year, representing a relatively dovish expectation among major central banks. In contrast, the People’s Bank of China set the one-year Loan Prime Rate (LPR) at 3.0% and the five-year-plus LPR at 3.5% on August 20, 2025, unchanged for three consecutive months. Some analysts suggest that the timing for further rate cuts or reserve requirement reductions in China may be delayed. This divergence in global policy provides differentiated opportunities for applying the 60/40 strategy across regional markets.

Strategy Optimization Path

In the complex market environment of 2025, a static allocation of 60% equities and 40% bonds is no longer sufficient to achieve optimal returns, making strategy optimization a key factor for profitability. From a global asset allocation perspective, the strong performance of non-U.S. markets challenges the notion of “U.S. exceptionalism,” prompting investors to reconsider the geographic distribution of the equity portion.

Some analysts highlight that investment opportunities outside the U.S., particularly in South Korea, are attractive for long-term investors willing to tolerate short-term volatility. Current valuations of Korean technology companies provide compelling entry points.

For the bond portion, duration management and credit selection are more important than simple proportional allocation. PIMCO recommends that investors avoid direct exposure to long-term Treasuries, as worsening U.S. fiscal conditions can put pressure on long-term bond auctions, requiring higher yields. In contrast, intermediate-term bonds, such as five-year Treasuries, are preferred, offering both relatively high coupon income and potential price gains during a rate-cut cycle.

The moderate inclusion of alternative assets can effectively complement traditional strategies. Gold has performed exceptionally in 2025, with year-to-date gains of up to 28%. Analysts suggest that core factors, such as U.S. dollar credit risk, will continue to support a gold bull market over the medium to long term, with an expected annualized return of around 8%, roughly in line with global nominal GDP growth. For traditional 60/40 investors, allocating 5%–10% of the portfolio to gold or other alternative assets can enhance resilience against inflation and rising geopolitical risks.

Source: TradingView

Sector and style allocations also require adjustment. In equities, WH Ireland Deputy Head of Research Ollie Clark recommends focusing on AI-related themes, which contributed to nearly a 23% gain in the S&P 500 in 2024. Meanwhile, Morningstar notes that with current U.S. equity valuations elevated, value stocks and small-cap equities could outperform again in the future, and stock markets in Europe, China, and Latin America remain relatively undervalued. This style rotation implies that investors should optimize the internal structure of their equity holdings while maintaining the overall allocation proportion.

Investor Insights

For different types of investors, the application of the 60/40 strategy in 2025 should be tailored, with key adjustments based on individual risk tolerance, investment horizon, and return objectives.

For younger and long-term investors, who generally have higher risk tolerance and longer investment horizons, maintaining or moderately increasing the equity allocation can be considered. However, emphasis should be placed on broadening global diversification to reduce overreliance on the U.S. market. In 2025, global equities show significant divergence, with European markets performing strongly and emerging as one of the top-performing regions, while U.S. equities face multiple challenges and comparatively weaker performance.

Historically, in the four instances when non-U.S. equities outperformed U.S. equities, three of them continued to outperform in the remaining three quarters of the year, with an average excess return of around 5 percentage points. This historical pattern suggests that the strong performance of non-U.S. markets in 2025 may have the potential to continue.

Near-retirement or risk-averse investors should consider a bond-tilted allocation. Public fund provider Vanguard recommends adjusting portfolios to a “40% equities + 60% bonds” structure. Bond allocations should be carefully constructed, focusing on intermediate- and short-term bonds as well as high-quality credit, while avoiding long-term Treasury exposure. These investors can also consider increasing allocations to defensive sectors, such as healthcare, consumer staples, and utilities, which have relatively stable demand and are less sensitive to economic cycles, helping to reduce overall portfolio volatility.

Regardless of the allocation ratio, a disciplined rebalancing mechanism is key to strategy success. Market volatility has intensified in 2025, and faster stock-bond rotation further underscores the importance of systematic rebalancing.

Investors can monitor two key indicators: first, the equity-risk premium (ERP), where an ERP exceeding two standard deviations signals an imbalance in stock-bond allocation and the need for rebalancing to restore optimal asset proportions; second, changes in Treasury futures positions, where a consecutive three-day increase exceeding 10% may indicate a shift in market sentiment, prompting investors to consider portfolio adjustments.

For investors seeking enhanced returns, tactical adjustments can be added to the classic 60/40 framework. At the sector level, allocations to technology growth areas such as AI and semiconductors may be considered, as the surge in AI computing demand in 2025 is expected to boost the semiconductor market. Using instruments such as the SPDR Portfolio S&P 600 Small Cap ETF to target undervalued small-cap segments is also feasible, as small-cap equities may offer more value opportunities amid elevated U.S. stock valuations.

In the commodities space, industrial metals such as copper have long-term investment potential due to energy transition and AI-related demand. Although prices have recently fluctuated amid economic growth concerns, the long-term trend of increasing demand remains clear, preserving their investment value.

Disclaimer: The content of this article does not constitute a recommendation or investment advice for any financial products.

Email Subscription

Subscribe to our email service to receive the latest updates