American Water Works: Long-Term Growth and Defensive Value from a Dividend King

![]() FoolBull

FoolBull

03:05 August 24, 2025 EDT

Key Points:

AWR generates highly visible, low-volatility cash flows through its regulated water and power businesses and long-term military contracts. The company has increased its dividend for 71 consecutive years, with a current dividend yield of approximately 2.7%, a decade high. This healthy payout ratio and cash flow coverage demonstrate the company's strong dividend sustainability.

Core growth comes from three aspects: 1. Recoverable capital expenditures under the California regulatory framework (pipeline network renewal, drought resistance and water quality compliance, wildfire resilience projects) drive rate base expansion; 2. Approved rate increases and surcharge mechanisms improve the matching of revenue and cash recovery; 3. Military contracts and new service areas provide long-term, stable incremental cash flow.

Risks focus on environmental and compliance requirements such as drought, wildfires, PFAS, capital expenditure and project execution risks, and financing pressures from rising interest rates. Current valuations (forward PE ratio ~22.5x) are at the lower end of their historical range, and the decline in share prices has brought them closer to reasonable or slightly undervalued levels. Overall, this utility stock is a defensive, long-term investment with high value.

American Water Works is a regulated public utility company with water and electric subsidiaries in California. It also provides water supply and wastewater treatment services to many military bases across the United States through long-term contracts. The current dividend yield is approximately 2.7%, which is at a relatively high level in more than a decade, and the valuation is also relatively moderate. The company has increased its dividend for 71 consecutive years, and has the dual identities of "Dividend King" and "Dividend Aristocrat", setting the longest dividend growth record among listed companies, and the stability and sustainability of dividends are significantly visible. In an environment of relatively friendly regulation and considerable interest rate expectations, AWR's regulated assets and contractual cash flows provide support for its earnings and dividends. Considering the dividend level, valuation and cash flow characteristics, the company has long-term allocation value.

Water use in the United States

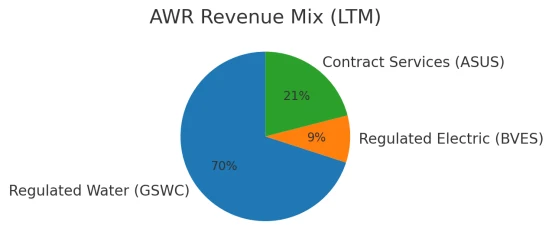

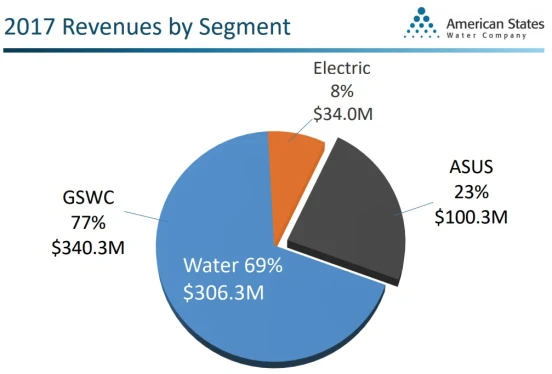

Founded in 1929 and headquartered in California, American State Water Company primarily operates in the regulated water supply business and provides electricity services. It also provides water supply and wastewater treatment to numerous military installations across the United States through non-regulated businesses. The company operates through three subsidiaries: Golden State Water Company (GSWC), Bear Valley Electric Services (BVES), and American State Utility Services (ASUS). AWR currently serves approximately 264,000 water/wastewater customers and 24,900 electricity customers, and has signed 50-year contracts with 12 military bases and a 15-year contract with one base. The company's total revenue in 2024 exceeded US$595 million, and its revenue in the last 12 months (LTM) was approximately US$616 million; approximately 70% of this came from the regulated water business, approximately 9% from the regulated electricity business, and the remainder from ASUS (non-regulated military water and wastewater contracts).

AWR's core operating foundation is California's regulatory system. Rates for GSWC and BVES are approved by the California Public Utilities Commission (CPUC) during the General Rate Case (GRC) cycle. This approval process is based on the regulatory asset base (Rate Base), allowable capital costs, a reasonable equity-debt structure, and accruable costs. Various balancing accounts are used to compensate for fuel/chemical costs, sales volume deviations, and other factors during the review period. This mechanism provides the company with a certain degree of cost recovery during periods of inflation, demand fluctuations, or interest rate fluctuations, but it also means that the rate of return and the cadence of returns depend on the review schedule and approval results. In its power business, BVES is subject to California's regulatory requirements for wildfire mitigation, distribution network hardening, and clean energy access. Capital expenditures and cost recovery are also achieved through GRC and special applications. Overall, the cash flow characteristics of regulated businesses are "low inelasticity and highly visible." Continuous capital expenditures drive rate base expansion, which in turn translates into accrued income in the next review.

ASUS's military contracts provide the company with a secondary source of cash flow, differentiated from its regulated assets. Most of these contracts have a 50-year term and are executed based on a "base service fee + operations and maintenance reimbursement + on-demand capital improvement work orders." These contracts typically include inflation adjustment clauses and are governed by service level agreements (SLAs) governing performance. Unlike regulated assets, the collection and profit of military contracts are more influenced by contract terms and the pace of work order approvals. However, their long terms, high customer concentration, and low credit risk help smooth the impact of economic cycles and demand fluctuations. The cross-base portfolio also diversifies the risk of individual projects. As the renovation and standardization of water systems at military facilities progress, ASUS's capitalized investments from work orders will continue to translate into returns and earnings over the contract period.

The company's future organic growth will primarily revolve around "accountable capital formation and recovery." For the water sector, capital expenditure and rate base growth will be primarily driven by aging pipeline replacement, storage and distribution facility renovations, water quality compliance and PFAS (per- and polyfluoroalkyl substances) management, drought mitigation and resilience projects, and automated metering (AMI) and leakage management. Amidst frequent droughts and extreme weather events, backup water sources, zoning regulation, and emergency dispatch also enhance system reliability and regulatory acceptance. Capital expenditures for the power sector will focus on wildfire risk mitigation (conductor insulation, vegetation management, sectionalizing switches and automation), distribution network upgrades, and distributed resource access. For military contracts, new rounds of work orders and scope expansions will determine incremental growth in the non-regulatory sector. Once these capital formations enter the valuation base or contract recovery cycle, they typically translate steadily into operating income and cash flow over the medium term.

In terms of capital structure and shareholder returns, AWR is characterized by "stable dividends + stable investment." Its 71 consecutive years of dividend growth rely on regulated and long-term cash flows. While maintaining dividend sustainability, the company uses debt and equity instruments to align capital expenditure cycles, driving rate base expansion and contract collection. Rising interest rates increase financing costs and compress valuations, but the company can partially hedge against this through its cost of capital and fee mechanisms. Therefore, changes in interest coverage, net debt/EBITDA, fixed/floating interest rates, and credit ratings become key indicators for measuring dividend safety margins and reinvestment capacity.

Risk constraints primarily come from four areas. The first is regulatory uncertainty: if the GRC-approved ROE, capital structure, and rate design are lower than applied for, returns will be compressed. At the same time, water conservation policies, water efficiency targets, and tiered pricing may alter sales and water market conditions. The second is environmental and compliance pressure: new water quality regulations such as those for PFAS, prolonged droughts and extreme weather, wildfires, and earthquakes are driving up O&M and insurance costs, and requiring higher levels of capital investment and operational resilience. The third is project execution and permitting risk: large-scale water treatment facilities and distribution network projects are subject to the risk of time and cost overruns, and the progress of permit approvals can also affect the pace of capitalization and cash recovery. The approval and acceptance of military task orders are also critical nodes in the cash flow path. The fourth is the macroeconomic and financing environment: high interest rates and capital market volatility will affect external financing costs, which in turn will affect the investment pace and short-term free cash flow coverage.

Putting the above factors together, we can see that AWR's fundamentals can be observed over the long term through several types of indicators: first, regulatory progress and results, including the timetable for the next round of GRC, the approved capital cost and rate arrangements; second, the synchronization of capital expenditures with the rate base and its distribution across the three lines of water, electricity and military; third, operational quality, such as leakage rate, proportion of non-revenue water, frequency and restoration time of water and power outages, and conclusions of water quality compliance inspections; fourth, the task order reserves, conversion rate and scope expansion of military contracts; and fifth, the matching degree of financial soundness and shareholder returns, including interest coverage, net debt/EBITDA, fixed interest ratio, dividend payout ratio and free cash flow coverage of dividends. In terms of valuation implications, AWR pricing generally reflects the cash flow certainty of the "regulated utility + long-term contract" combination and the impact of the interest rate environment on the discount rate: when progress is made in regulation and project execution, the rate base expands, and dividend coverage is stable, the market tends to assign a higher certainty premium; conversely, interest rate shocks, low valuation results, or project delays may change the direction of valuation.

Revenue growth

American States Water (NYSE: AWR) announced its second-quarter fiscal 2025 results on August 7, 2025: revenue increased 4.9% year-over-year, from $155.3 million to $163 million. Revenue increased in both the water and power segments, while contract services declined due to reduced construction activity. Diluted adjusted earnings per share (EPS) were $0.87, $0.04 below consensus estimates, primarily due to weaker contract services revenue and profits; a slight increase in diluted share capital also diluted the per-share basis. The company guided that 2025 earnings growth would be driven by approved water and electricity rate increases and continued infrastructure investment. The stock price has fallen approximately 3.85% year-to-date and approximately 9.22% over the past 12 months.

From a long-term perspective, the company's revenue is projected to increase from $459 million to $595 million from fiscal years 2015 to 2024, showing an overall upward trend. Despite disruptions from drought and declining water use, organic growth was achieved through capital expenditure recovery, rate increases, and regulatory-approved surcharges. In January 2025, the California Public Utilities Commission (CPUC) approved water rates for 2025–2027 and electricity rates for 2023–2025, which are expected to increase the rate base and medium- to long-term revenue. The current allowed return on equity (ROE) is 8.85% for GSWC and 10.0% for BVES.

The company's expansion is not primarily based on mergers and acquisitions. Instead, its non-regulated military contract services business is steadily expanding through new bases and projects. Recent progress includes the signing of a 15-year water/wastewater contract with Joint Base Cape Cod, Massachusetts, in 2023, which will help enhance revenue visibility and cash flow stability. Overall, the rate structure of its regulated business and long-term military contracts contribute to profitability, while near-term revenue generation primarily stems from the construction pace of its contract services and dilution.

The current long-term growth momentum of US state water utilities remains risky. Driven by an expanded rate base and rate increases, the market expects the company's revenue to increase by approximately 9.62% year-over-year in fiscal 2025 and by approximately 3.98% in fiscal 2026. Under California's relatively friendly regulatory framework, capital investment and rate mechanisms are expected to be further optimized, particularly for the Golden State Water Company (GSWC) segment, where the rate base has maintained an annual growth rate of approximately 10% in recent years. The company is increasing capital investment to address service disruptions and safety risks caused by aging infrastructure, drought, and wildfires. Meanwhile, pending privatization of military bases provides a channel for further expansion of its non-regulated business. The company also continues to expand its service area in California, recently reaching an agreement with a developer to add approximately 1,300 new water and wastewater connection points.

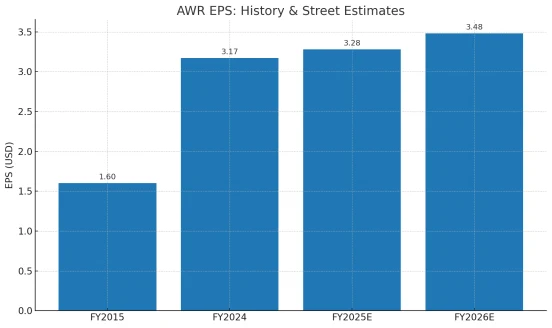

In terms of profitability, adjusted earnings per share have increased from $1.60 in 2015 to $3.17 in fiscal 2024. Consensus estimates indicate that EPS is expected to increase by approximately 3.47% year-over-year to $3.28 in fiscal 2025, and further by approximately 6.2% to $3.48 in fiscal 2026. EPS has averaged approximately 7.2% annually over the past five years. Driven by California's rebounding population growth and increased user connections, earnings growth is expected to remain in a similar range, coupled with the potential contribution from new or renewed military base service contracts. It is important to note that the company has not implemented large-scale repurchases to hedge against equity dilution. In recent years, it has issued a modest amount of additional shares to match capital expenditures, which has put some pressure on per-share growth.

risk

American States Water (AWR) currently faces core operating risks stemming primarily from both natural and policy constraints. First, drought and wildfires remain long-term variables for California utilities. Drought-induced water withdrawal restrictions and mandatory water conservation are suppressing water consumption under metered billing. Wildfires are also putting pressure on its electric utility subsidiary (BVES)'s transmission and distribution network, operations and maintenance, safety, and insurance costs, potentially triggering more frequent public safety power shutoffs (PSPS) and additional mitigation capital expenditures. While the company has accumulated experience in emergency response, asset reinforcement, and dispatch over the past few years, the increasing frequency and intensity of extreme weather events could still lead to intermittent service disruptions, claims, and regulatory scrutiny, driving up operating and financing costs.

On the competitive front, AWR's regulated water and electricity distribution businesses enjoy natural monopoly status within their franchise areas, with pricing and investment returns primarily governed by the California Public Utilities Commission (CPUC) and related regulatory frameworks. While competitive bidding is currently underway for its unregulated military water and wastewater contracts, the long-term nature of these contracts and their inflation-adjusted clauses provide some support for revenue and cash flow. However, military contracts still present renewal uncertainties, project execution and cost control risks, and potential volatility due to the government's "termination for convenience" clauses.

Regarding costs and capital expenditures, tariffs and fluctuations in bulk material prices (such as concrete, steel, copper wire, valves, transformers, and conductors), coupled with labor and contractor shortages and lengthening supply chain cycles, could also raise unit investment costs and increase the risk of project delays. Regulatory lags and timing differences in tariff implementation could lead to a misalignment between cash collection and capital expenditures. Regarding interest rates, utilities rely on long-term debt and preferred stock/additional offerings to support capital plans. A tightening financing environment would compress interest margins and create dilution pressure on per-share earnings. While returns (ROE/weighted cost of capital) may adjust over subsequent rate periods, short-term cash flow and credit metrics may remain under pressure.

Compliance and environmental risks also exist. The ongoing tightening of drinking water quality standards (e.g., increased requirements for the detection and treatment of trace pollutants and persistent organic pollutants (PFAS)), tightened groundwater management, and updated water permits are all likely to result in capital investment and operating expenses for new treatment facilities, recycled water, and emergency water projects. Furthermore, energy efficiency, emissions reduction, and wildfire mitigation programs (WMPs) increase fixed costs on the electricity side. While most compliance-related investments can be recovered through rates and surcharges, there remains uncertainty regarding approval timing, cost approval, and project review. Compliance and data risks in cybersecurity, billing systems, and third-party outsourcing are also increasing, requiring continued investment to reduce incident rates and handling costs.

In terms of demand and social factors, California's population and industrial mobility, water conservation culture, and price elasticity have led to a downward trend in water consumption per user. Some regulatory mechanisms (such as balancing accounts and differentiated recycling) can help mitigate the impact of sales fluctuations on revenue, but they do not fully offset it. Adjustments to supply priorities during periods of extreme heat or drought may also alter short-term water usage structures and cost curves.

Overall, AWR's risk mitigation comes from three approaches: first, mitigating the impact of extreme events through proactive capital planning and asset hardening (fire-resistant conductors, pipe network upgrades, backup water sources, zoning metering, and leak control); second, maintaining frequent interactions with the CPUC and local water utilities to shorten rate review cycles, optimize allowable returns and catch-up mechanisms, and reduce regulatory lags; and third, strengthening project and financing management, smoothing interest rate and material cost fluctuations through a longer-term, more diversified funding structure and hedging strategies. Investors should continuously monitor high-frequency indicators including service reliability and incident rates during drought and wildfire seasons, annual capital expenditure execution and unit costs, rate case progress and allowable return updates, bad debt and collection rates, changes in insurance coverage and retention, and the pace of military contract renewals/additions. These variables will determine the company's earnings quality and free cash flow stability within its "high investment, strong regulation, and high resilience" framework.

Competitive Advantage

American Water Services (AWR)'s competitive advantage stems primarily from its regulated "natural monopoly" position within its franchised service area. Its water supply and distribution network features strong economies of scale and sunk costs (pipelines, water collection and distribution facilities, stations and lines, and water and land use permits are all asset-heavy and require long-term investments), making it difficult to replicate a second set of infrastructure within the same geographic area. The supporting regulatory framework, through rate cases and surcharge mechanisms, allows the company to recover qualified capital and earn reasonable returns under regulatory compliance, thereby transforming high fixed costs into predictable cash flow. A second competitive advantage stems from long-term military utility privatization contracts. ASUS's multi-year water/wastewater service agreements with numerous military bases incorporate inflation adjustments, capital improvements, and operations and maintenance provisions, ensuring high revenue stickiness and visibility, mitigating cash flow disruptions from macroeconomic fluctuations and regional demand fluctuations.

Source: simplysafedividends.com

This combined advantage reinforces each other across operations, finance, and compliance. On the operational side, AWR's long-standing engineering and O&M capabilities (including zoning metering, leakage control, access to unconventional water sources, and power supply and distribution safety during wildfires and extreme weather events) reduce unit O&M costs, improve network reliability, and enhance service ratings under regulatory assessments. On military projects, standardized project management and compliance review processes enhance the efficiency of executing incremental upgrades and change orders. On the financial side, the "rate-base-return" mechanism of regulated businesses and the long-term nature of military contracts jointly support stable free cash flow conversion and access to capital market financing. This enables the company to continuously invest in asset hardening and expansion, driving rate base expansion and economies of scale, creating a virtuous cycle of "investment-recovery-reinvestment." On the compliance side, frequent interactions with regulators and a strong track record of compliance enhance the feasibility of rate reviews, retroactive items (surcharges, allowance accounts), and the inclusion of new regions. On military contracts, consistent performance compliance and audit traceability help maintain eligibility for continued contracts and new project additions.

AWR's competitive advantage also lies in the scalability of its "entry points and boundaries." Its regulated water subsidiary in California is gradually increasing its connections through new development zone access, grid connection agreements, and concession adjustments, marginally amplifying fixed network utilization and amortization. Its military business, leveraging its existing contract performance record, is participating in more base privatization bids or subsequent renovation projects, increasing unit customer contribution through incremental capital projects and expanded service scope within the same contract period. Furthermore, "institutional resources" such as water rights and abstraction permits, recycled water facilities, and regional interconnection projects have become differentiated supply security assets in an environment characterized by more frequent droughts and climate events, increasing customer and regulatory reliance on its platform from the supply side.

From a sustainability perspective, this competitive advantage is not static but depends on the ability to manage three key constraints: First, the cyclical adjustments of regulatory terms and permitted returns. Companies need to minimize regulatory lags and maintain reasonable ROE/WACC through accurate cost attribution, project justification, and public interest proof to ensure investment returns and stable cash flow. Second, the pass-through of compliance investments and cost inflation. As new drinking water standards (such as PFAS) and wildfire mitigation (WMP) requirements rise, ensuring the approval and timely recording of compliant capital expenditures and operations and maintenance costs is a prerequisite for protecting the company's moat from cost erosion. Third, resilience to extreme climate and supply chain risks. Through asset hardening (fire-resistant conductors, undergrounding, backup power sources), multi-source water supply deployment, long-term material procurement, and insurance and reinsurance combinations, the impact of a single incident on service and finances can be reduced, safeguarding the "reliability-compliance-cash flow" triangle.

In summary, AWR's core advantage lies not in short-term "price competition" but rather in the impact of its "rules-based moat" comprised of institutionalized network assets, compliant recovery mechanisms, and ultra-long-term contracts. This moat transforms high fixed costs, strong regulation, and public service attributes into predictable cash returns over the medium to long term, forming a closed loop with the continued expansion of its rate base and new connections. At the execution level, operational reliability and compliance performance are key factors in sustaining and strengthening its advantages in an increasingly stringent climate and regulatory environment.

Dividend Analysis: Three-Line Verification of "Cash Flow - Regulation - Balance Sheet"

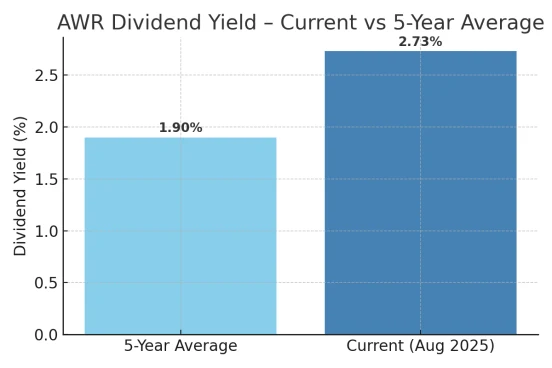

American Water Works (AWR)'s stock price has weakened over the past six months, pushing its dividend yield up to approximately 2.7% , significantly higher than its five-year average of approximately 1.95% . Historically, a higher initial yield often indicates a higher proportion of dividend contributions in long-term returns; however, whether this translates to a "cheap valuation" remains dependent on variables such as the interest rate environment and regulatory certainty.

AWR has increased its dividend annually for 71 consecutive years , making it one of the few utility stocks to hold the distinction of "Dividend King" or "Dividend Aristocrat." Its dividend has grown at a compound annual rate of approximately 9.1% over the past five years and approximately 8.0% over the past ten years . The company has already implemented a quarterly dividend increase of approximately 8.3 % through 2025. Based on the consensus EPS estimate of approximately $3.33 for fiscal 2025 , the payout ratio (Div/EPS) is approximately 57% , which is within the median range for the regulated water industry and below the 65% threshold generally considered "high." Regarding cash flow, operating cash flow (OCF) is projected to increase from $112 million in fiscal 2020 to $199 million in fiscal 2024 , providing stable coverage for the dividend. If we assume that OCF in 2025 is US$150 million and the annual cash dividend is approximately US$75 million , the cash dividend/free cash flow ratio will be approximately 50% ; in the utilities sector, this coverage is a better safety attribute (the actual value will vary with fluctuations in capital expenditures and working capital).

Regarding the company's balance sheet, it maintains an investment-grade "A" credit rating. According to disclosures, the leverage ratio, corresponding to debt and interest burden, is approximately 3.8x, and the interest coverage ratio is approximately 4.0x , comparable to most regulated peers. For hydropower utilities operating under a "rate-based-recovery" model, the key is not the absolute debt size, but rather the debt duration structure and the isolation of interest rate risk. For example, a higher proportion of long-term, fixed-rate debt can keep the erosion of dividend payout capacity within manageable limits due to rising interest rates. Conversely, a greater reliance on rate cases and catch-up provisions is necessary to hedge against rising financing costs. Regarding third-party quantitative assessments of dividend quality , AWR scores high in several comprehensive scoring systems (such as the A+ rating in the "Portfolio Insight" framework), reflecting the consistency of earnings, cash flow, dividend record, and financial resilience.

Valuation

From a valuation perspective, AWR's valuation has declined with the weakening stock price and downward revisions to its 2025 forward EPS forecast. The current forward P/E ratio is approximately 22.5x , below its 5- and 10-year range averages. The consensus estimate for fiscal 2025 adjusted diluted EPS is approximately $3.33 (an increase of approximately $0.16 from 2024). Given economic uncertainty and the potential impact of the California drought and wildfires on cost and rate lags, a relatively conservative forward P/E ratio of 23x represents a "fair value" of approximately $76.59 . Compared to the current share price of $74.94 , the stock appears slightly undervalued . Further, a sensitivity range of 22–24x forward P/E ratios yields a fair value of $73.26–79.92 , implying that the current price is approximately 94%–102% of the fair value range .

Comparing this result with other frameworks, if a "hybrid fair value model" (combining earnings multiples with dividend yields) is used, the fair value may be more inclined towards the mid-to-high range; for example, some multi-factor models give a valuation of approximately $105 per share . Taking the median of the two methods, the fair value falls in the range of $90-91 , and the current price is significantly lower than this center. However, the consensus target price of the seller is approximately $81.5 , which is only about 9% premium to the current price ; the quantitative scoring model is conservative about its "valuation, profitability, and momentum", and the "growth and expectation revision" factor is relatively positive. The differences between different frameworks essentially reflect differences in three things: the pace of rate implementation, the efficiency of capital expenditure recovery, and the interest rate path.

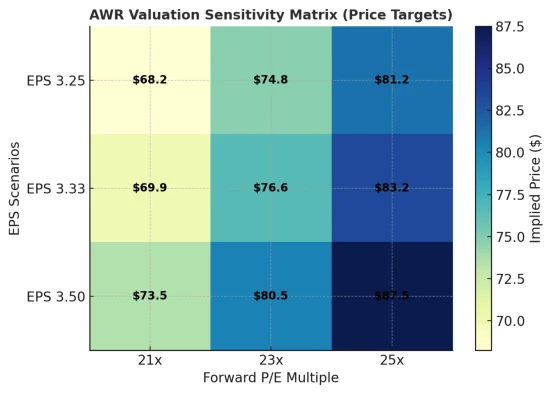

Three further points can be expanded upon. First, scenario-based valuation : Using a 2×3 grid formed by the dual dimensions of earnings and multiples better captures uncertainty. For example, the low/baseline/high EPS scenarios ($3.25/3.33/3.50) intersect with the multiple bands of 21/23/25, corresponding to a price range of approximately $68–88 . Upward penetration relies on improved visibility of cross-cycle ROE and rate-based growth (including PFAS and drought relief project recovery), as well as the "duration recovery" of utility stocks brought about by falling interest rates. Second, relative valuation anchors : Forward PE ratios for water/hydro-hybrid utilities in the same sector typically range from the high teens to the high twenties , with California peers often carrying a small premium due to regulation and capital intensity . AWR currently falls in the lower end of the band, indicating that discounts for "rate and extreme weather disruptions" are still priced in. Third, the return decomposition : If 23 times/US$76.6 is taken as the conservative fair value within 12 months, the central price contributes about +2%~3% , plus the forward dividend yield is about 2.7% . If the profit is realized and the multiple does not shrink, the one-year nominal total return center will be about 5% ; if the multiple returns to 24-25 times and EPS exceeds expectations, the return elasticity at the upper end of the range will increase significantly.

Constraints and catalysts that need to be emphasized simultaneously: (1) Regulation and rates - the speed of implementation of multi-year rate plans and surcharges/catch-up accounts directly determines the timing of cash recovery and the upper limit of valuation; (2) Capital expenditure and free cash flow - PFAS, drought relief and wildfire mitigation projects may put pressure on FCF in stages. If equity financing is used to support them, the unit shareholder return will be diluted; (3) Interest rate path - the decline in long-term interest rates usually raises the valuation center of the sector; conversely, it may suppress the multiple; (4) ASUS military contract and new connections in California - the visibility of new service areas and new military outsourcing contracts/additions is a "weak beta" factor that increases earnings per share and supports dividend growth. In summary, the current pricing is more like a " slightly discounted defensive stock ": downward support is provided by regulation and the dividend system, while upward support depends on the rate and capital recovery rhythm, as well as whether the disturbance of interest rates and extreme weather on operations and costs can be marginally alleviated.

Conclusion

American States Water (AWR) is a regulated water, wastewater, and electric utility that also provides long-term contract water and wastewater services to several U.S. military bases through a non-regulated entity.

Leveraging its regulated monopoly position within its specific service territory, robust operations, and prudent capital allocation, the company has achieved moderate but consistent organic growth over the past several years, fostering a virtuous cycle of "earnings growth, dividend increases, and reinvestment for expansion." The current share price pullback has placed its dividend yield at a relatively high level in nearly a decade. Combined with recently approved rate increases and a continuously expanding rate base, this simultaneous increase in dividends and earnings is highly sustainable. AWR's growth momentum stems primarily from three sources: first, regulatory-recoverable capital expenditures (including aging pipeline network upgrades, drought and water quality compliance investments, and wildfire-related resilience projects) have driven a rising rate base; second, California's rate cycle and surcharge mechanism have improved cash collection timing, reducing the mismatch between revenue and costs; and third, military base privatization projects and the addition of new service areas have provided long-term, stable contracted cash flows. As a regulated utility, AWR is relatively insensitive to macroeconomic fluctuations but more sensitive to interest rates: declining long-term interest rates tend to elevate its valuation. Key factors influencing mid-term performance are regulation and enforcement: the pace of rate implementation, capital expenditure recovery efficiency, and operating cost control directly determine the growth rate of free cash flow and earnings per share. Furthermore, any modest share issuance to match capital expenditures must be weighed against the potential dilution impact on per-share earnings. Key risks include operational disruptions and cost volatility caused by drought and wildfires, increased capital intensity and compliance expenses driven by water quality compliance requirements such as PFAS, delayed or slower-than-expected rate approvals, and pressure on project returns from rising material and construction prices.

Corresponding potential catalysts include the addition of new service areas or connections, the signing of more military base contracts, the unexpected completion of rate proposals, and a shift in the interest rate environment. Overall, AWR offers both dividend stability and growth visibility, making it a suitable long-term dividend growth-focused investment during periods of declining valuations and rising yields, smoothing portfolio volatility and enhancing compounding efficiency through reinvestment.

Disclaimer: The content of this article does not constitute a recommendation or investment advice for any financial products.

Email Subscription

Subscribe to our email service to receive the latest updates